The Changing Structure of the VC Industry

Much of the discussion on the changing structure of the venture capital industry in the past few years has focused on just one element: the rise of crowdfunding platforms and new entrants to the earliest funding stages of our market. Yet a broader look will show that changes are afoot in the entire value-chain of the financing of startup companies shifting more dollars and more value captured from public financings to private financings and creating new competition in late-stage financing.

A look forward, not backward

Just a few years ago the narrative in the venture capital industry was that performance over the past 15 years was poor and that venture wasn’t an asset class worthy of limited partner’s investment. As I pointed out in presentation with much data, these analyses were flawed in that they considered only rear-view mirror data. The data set only considered only a period at the peak of Internet hype, with the launch of many over-capitalized businesses against a limited market size of consumers and businesses, and a venture capital industry that had tripled in size in just three years.

Where are we today?

- We have 2.4 billion Internet users, or 50x more than before.

- Online connections are 180x faster at 10.5 Mbps.

- 164m US smartphone users gives us “always-on” mobile connectivity

- We’re all socially connected, so great businesses spread faster.

- We all have one-click purchase power through Apple, Google, Amazon and eBay.

- The VC market has right-sized, returning back to mid 90’s levels with less competition.

- The cost to start a business is 95% lower, meaning many more companies are created and funded by angel and seed investors.

- It still takes venture capital to scale a business, which means large amounts of capital go into industry winners like Uber, Airbnb and Snapchat.

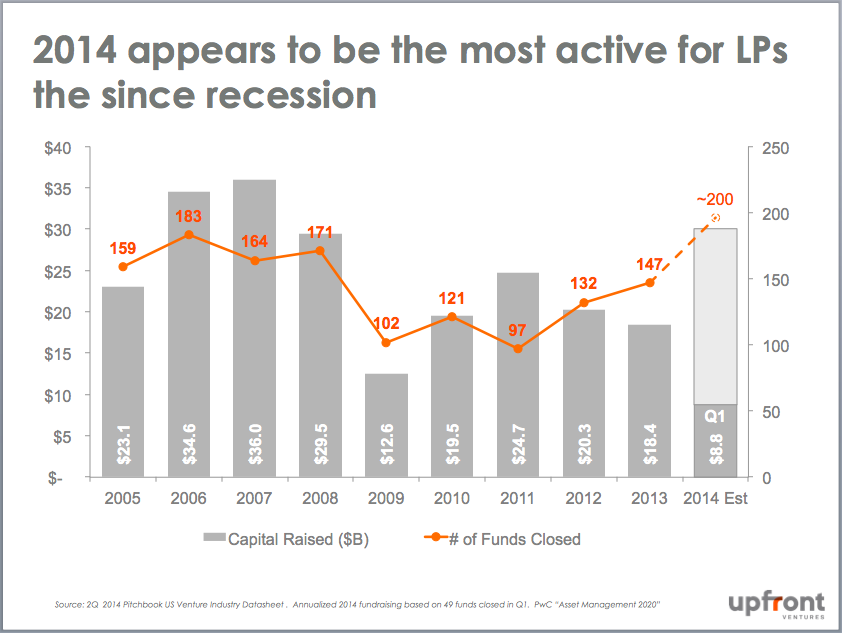

It doesn’t take a huge leap to see how well the VC industry is positioned for the immediate future. LPs have taken notice as 2014 is by all accounts the busiest year for LPs since the Great Recession began as it is forecast that between $25-30 billion to be invested in some 200 venture funds. Where will these dollars go and how is the industry changing?

Money Bifurcating into Small & Large

Just 3 years ago there was talk of LPs “not being able to write small enough checks” to fund seed-stage VCs. The new narrative is seed-stage is here to stay, but “will my seed funds be able to fund the prorata of their winners?” Stated simply — if you seed funded Uber at $4.5m pre-money valuation you certainly would want to exercise your right to continue investing if you had pro-rata rights. The race is on to plug this gap in the private markets.

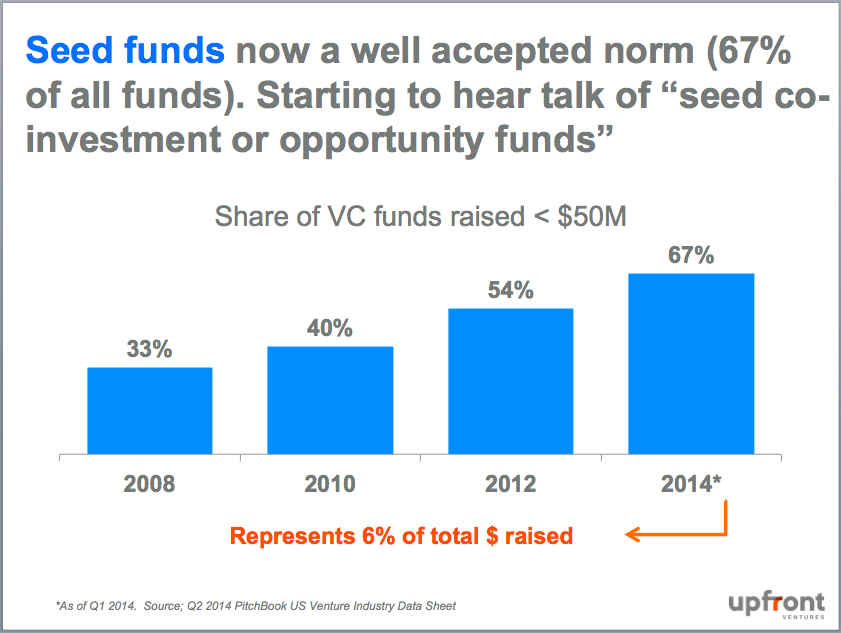

Seed funds now represent 67% of all funds being created now, which is up 100% from 6 years ago. And while it only represents 6% of the total capital of the VC industry — this is a meaningful shift in structure.

At the other end of the spectrum large funds have gotten even larger in the past few years which has massively increased the amount of consolidation in our industry as 66% of LP money into venture is now concentrated in late-stage or full-cycle VCs, which is likely $17-20bn in 2014.

Why is this?

- Many pension funds are simply too large to write small checks and favor the ability to write $50-100 million checks to funds. If you don’t want to be more than 10% of a fund that implies fund sizes in the $500 million-$1 billion range.

- Fund of funds (who take money from large pensions, sovereign wealth funds, etc. and break it into smaller sizes) often sell “access.” What they’re really saying is that they have the relationships to be able to invest in Sequoia, Benchmark, Greylock, Kleiner Perkins, Accel, etc. and the bigger funds often can’t get in directly.

Of course it’s much harder to identify “emerging managers” who it turns out have been some of the best performers over the past 5-7 years such as Union Square Ventures, Spark Capital, First Round Capital, True Ventures, Greycroft, Foundry Group, Thrive and Upfront Ventures. The challenge is that if you don’t get into the first 1-2 funds you don’t get in at all because they, too, become “over subscribed.”

The pioneering fund of funds realize that their source of differentiation is much more about getting into the newer market leaders than the established venture capitals since most historic fund-of-funds have some level of old-line access.

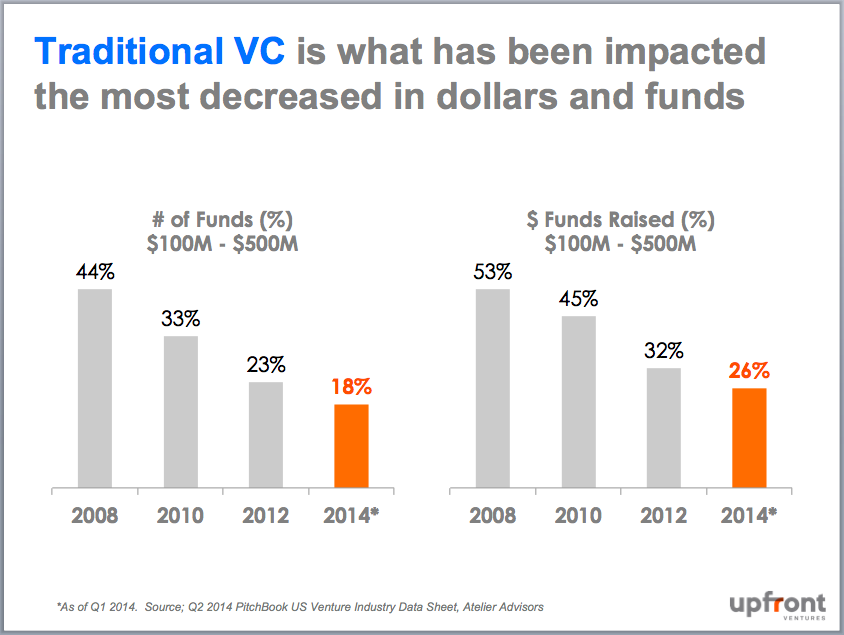

The most puzzling bit of data was that “traditional VC” — funds in the $100 million-$500 million range — seemed to be shrinking since the Great Recession in both numbers of VCs getting funded and in terms of total dollars in this class of VC and this seemed to fly in the face of the rise of successful emerging funds. By 2014, traditional VC would have halved in just 6 years in both number of funds and dollars allocated to category as dollars are shifting earlier & later.

But there is another major factor at play in the concentration of capital in larger funds: many traditional VC firms were now setting up “opportunity funds” or “growth funds.” The data ends up looking skewed towards larger funds when it actually involves traditional VC funds now geared up to take capture more of the value in private funds before they went public.

This is a structural shift in our industry few have talked about publicly.

The Opportunity Set Ahead

The trends of faster-growing startups due to social networking, credit card enabling and mobile-first consumers, show many startups becoming very large financially before needing to go public. Many of them could be profitable if they chose to. But markets value high growth over short-term profitability. As long as private-market capital is available, these companies would rather remain private for longer before going public.

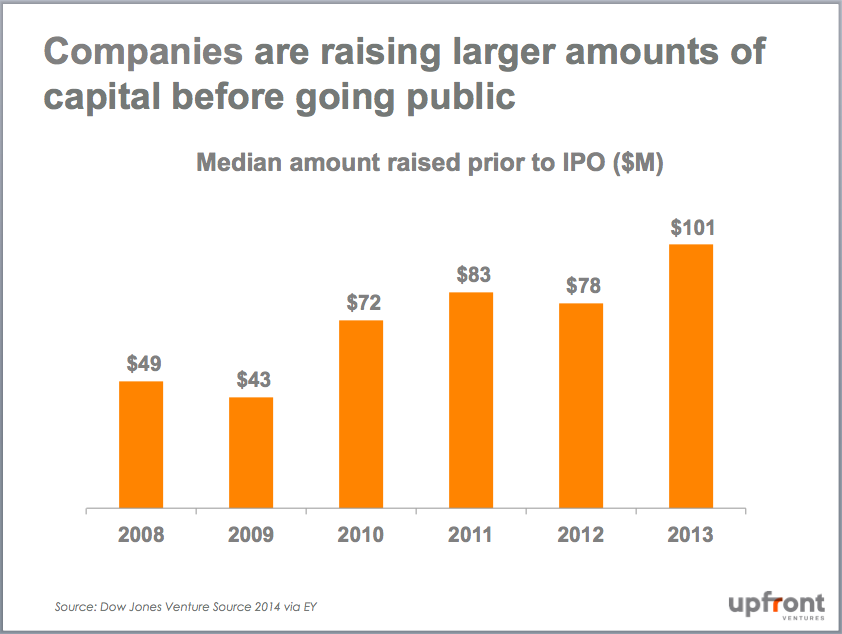

Thus, the amount of money that companies have raised before going public doubled since the Great Recession from $49 million median financing pre-IPO to $101 million in 2013. The overall trends in our industry have breathed a new life into the venture capital industry. From a period of veering off target with the laziness & riches of the dotcom era, our industry has righted itself.

The biggest changes in our industry have been driven by technical changes themselves to which venture capitalists are observers and fortunate beneficiaries. I highlighted how these tectonic technical shifts have altered the VC industry in this post: How Open-Source & Horizontal Computing Spawned the Micro VC Market. 2007 was the watershed year. Facebook went mainstream after the F8 conference and its big push beyond college campuses. Twitter spread through the tech crowds at SxSW and raised its first venture capital round led by Fred Wilson. The iPhone was released.

The seeds of cheap cloud computing, social networking & mobile were planted and then the 2008 financial crisis brought a hurricane that swept much of the old, dead brush from the venture capital industry and ushered in a new phase perhaps best punctuated by Sequoia’s famous and now ironic 2008 presentation “RIP Good Times.” The “big boom” in startup financing started around March 2009 — more than 5 years ago — and hasn’t abated.

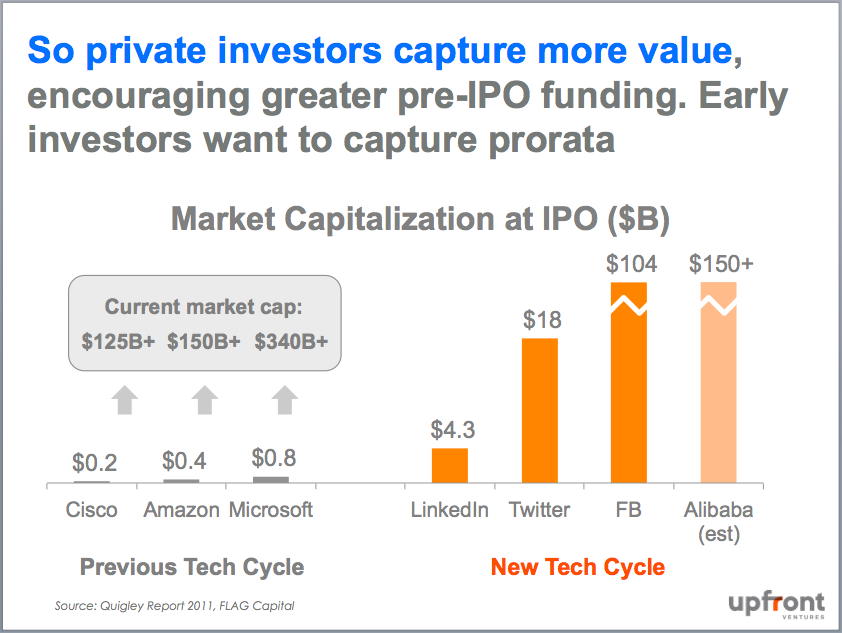

Cheap, mobile, social, global, massive, always-on, one-click-purchase has led to the most successful companies of our era hitting unprecedented scale early in their development and has massively shifted the value captured from post-IPO investors to pre-IPO investors. Whereas the market caps of Cisco, Amazon and Microsoft at IPO were $200 million, $400 million and $800 million respectively, the market caps of LinkedIn, Twitter and Facebook were $4.3 billion, $18 billion and $104 billion. Thus the rapid rise of DropBox, Airbnb, Pinterest, Maker Studios, Uber, Lyft, SnapChat, Tinder, Waze, KickStarter and so many more great standouts that have been a boon to private-market investors.

From a technology perspective, our journey is nowhere near over. Even the most somber of industry analysts must acknowledge that the shift from computers as devices controlled by humans to smart devices that are all computers connected to an Internet cloud — the so-called “Internet of Things” — is breeding massive new opportunities. Just see the growth of Dropcam, GoPro and Nest for the tip of the iceberg in what is to come.

Of course, the strongest industry players don’t stand still.

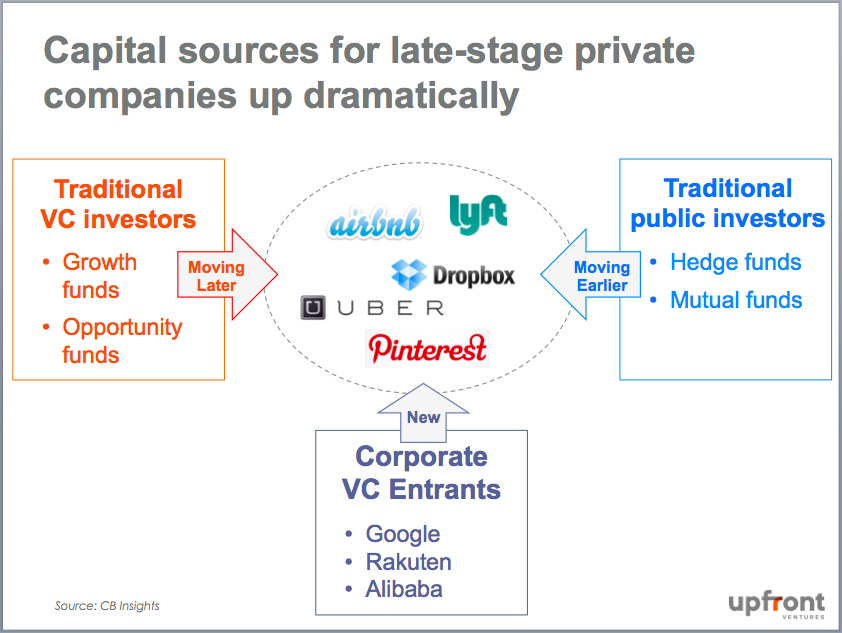

Early-stage VCs have realized that they need to capitalize on this trend, which is why many traditional VCs have set up “opportunity” funds that sit alongside their core funds as a means of capturing more private-market (pre IPO) value. Opportunity funds typically have better economics for the LPs who invest in them.

Traditional VC isn’t being gutted — it’s being supplemented.

Many prominent LPs have also recognized the “pro rata opportunity” and have set up “direct investment vehicles” themselves to take pro rata stakes in their managers portfolio companies. Expect this trend to continue. The biggest response to the public-turned-private value capture, however, has been the push for public market investors to move into the private sphere. Public-company tech investors creates competition in late-stage financings and these investors can afford to be less price sensitive if they choose.

The value capture in the private markets has also led some hedge funds and other major non-private-market investors to become late-stage VCs. Many of these investors lack the skills, focus, experience and temperament to make great, patient, long-term, private-market investors. Trying to shoe-horn a hedge-fund mentality into venture capital markets cannot portend a happy outcome. Marc Andreessen captured some of this sentiment in his recent “10 Ways to Damage Your High-Growth Tech Startup” Tweetstorm.

When the tech markets goes through their next inevitable bear cycle, every public market investor will return to their day jobs and abandon the hard work of rebuilding and restructuring the remaining over-capitalized companies. We saw this movie already after the dotcom collapse and the sequel will be no different. Publics sold many of their positions to secondary investors. It’s hard to work out the cap table with your peers when one of them has no real intent in fixing the problem.

Why do VCs stick around and fix problems in a massively changing financial market? Because this is all VCs do, and if we intend to work with all of our fellow VCs and entrepreneurs when the rain ends and the sun shines again, our reputations matter greatly. This “game theory” of mutual interests in collaboration — even as we occasionally compete fiercely — is what forces better behavior in our industry than otherwise might exist.

The result of these new market trends of pro rata takers, corporate investors and public market entrants has led to a sharp spike in the valuations of late-stage financings. While this might not matter for the industry’s best companies, the definition of what is “best” will clearly be stretched as people compete to get in on perceived great deals.

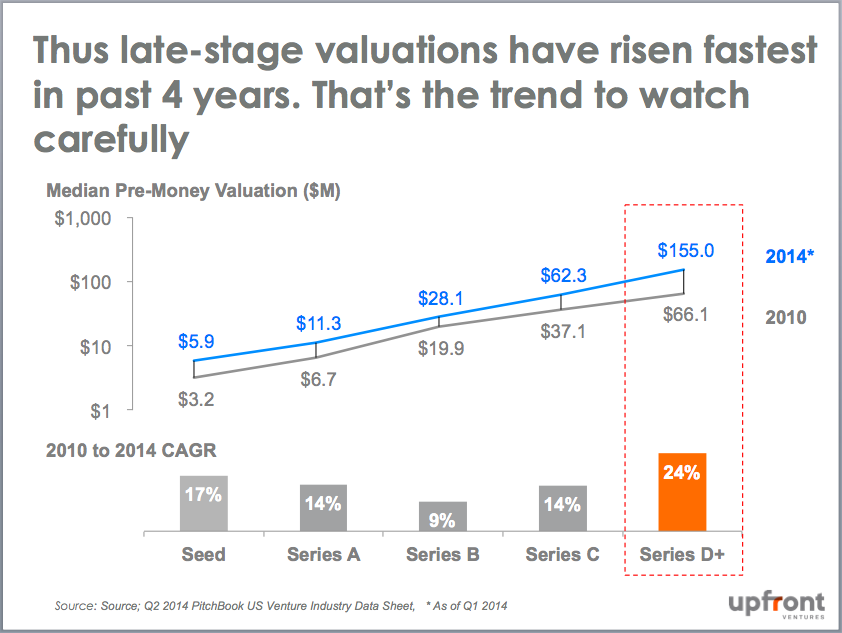

Venture capital valuations are up across every segment of the industry as can be expected by our 5-years of growth markets but they are up most pronounced in the late-stage financings. There, the median valuation has risen from $66 million in 2010 to $155 million in 2014 (a 24% compound annual growth rate).

But about that “bubble” we always hear about?

It certainly doesn’t yet seem to be the case regarding private tech market companies going public. Not only are they going public later, when they are larger & stronger, but the valuations upon their debuts are significantly more rational than the public dotcom bubble. From DotCom 1.0 to now we have seen the following: Years to IPO went from 3.1 years to 7.4, revenue of a startup at IPO went from $35m to $102m, and the valuation (market cap / revenue multiple) went from 13.3x to just 5.3x. Certainly the public markets for now are more rational than the last time around.

Summary

Cheap, mobile, social, global, always-on, one-click-purchase leads to unprecedented revenue growth and companies staying private longer. That means there are more opportunities than ever in history for venture capital firms and lots of new entrants moving to capture this value. All of that means there are amazing opportunities, risks and uncertainties for the coming decade.