It was the sale Scott Nuttall had to make. On a Saturday morning in April 2013, Nuttall was sitting at a corner table in the nearly empty restaurant at the Hilton in Short Hills, N.J., striving to persuade his burly guest to trade one of the best jobs in banking for a chance to rescue one of the hardest of hard cases.

For Nuttall, the recruiting mission was personal, even emotional. Six years earlier he’d led the nearly $30 billion leveraged buyout of First Data (FDC), a payments-processing colossus, for KKR, the legendary firm where Nuttall serves as chief of asset management. Since then, First Data had met failure at almost every turn, churning through CEOs along the way.

Nuttall was so determined to hire the star manager sitting at his elbow that he’d canceled a vacation to Italy for his wife’s 40th birthday to arrange this meeting. “She said that we’ll have a lot less stress if you find the right CEO … so go ahead and cancel,” recalls Nuttall. “I knew this hire could be the difference between the greatest success or failure I’ve been part of at KKR.”

The prize candidate was Frank Bisignano, co-COO of J.P. Morgan Chase and a bulwark of the Jamie Dimon–led team that revitalized that bank. As they breakfasted on omelets, Nuttall stressed that First Data might perform better if it got smaller and more focused. KKR (KKR) planned to sell big pieces of the $11 billion company. “First Data may just be too big and complex for any one person to run,” Nuttall said.

Bisignano’s response amazed his host. “Don’t sell anything!” he told Nuttall. Bisignano said that First Data’s immensity could prove its biggest asset. “Whatever you’re thinking of selling, I can fix it,” he said. “It will take an A-team, and I’ll field one.” And he argued that First Data—best known, when it was known at all, for the unglamorous work of routing your charges when you swipe a credit card at the gas station or corner deli—could reinvent itself as a tech juggernaut. The key to the transition, Bisignano said, was in his pocket. He held up his iPhone and declared, “First Data can be to merchants what this device is to millions.”

By the time luncheon BLTs arrived, Nuttall had landed his CEO. And the leader Nuttall describes as a “force of nature” had sold him on a cultural upheaval that could turn the industry’s lumbering warhorse into a breakout innovator—one that would compete with Silicon Valley unicorns to bring big data to small businesses.

But before Bisignano could pursue that plan, he had to address a textbook case of a leveraged buyout gone wrong. KKR’s LBO had turned First Data into one of the most heavily leveraged companies in America, saddling it with hefty interest payments just as revenue growth leveled off because of the effects of the Great Recession. Smaller, nimbler competitors were poaching customers by offering lower fees and, often, better technology. The company was en route to posting its sixth consecutive annual loss; by the time Nuttall met Bisignano, KKR valued its stake in First Data at just 60¢ on the dollar.

What’s more, Bisignano inherited a workforce that had never before experienced a drop in sales—and sometimes seemed either too paralyzed or too lackadaisical to confront it. Not long after becoming CEO, Bisignano recalls, he visited First Data’s biggest operations facility—an outpost in Omaha, full of ardent University of Nebraska football fans. Straining to light a fire under the staff, he told them, “If the University of Nebraska had a 2–10 season, how would you feel? That’s how First Data has been doing!”

These days, First Data is no longer a laggard. The 56-year-old Bisignano is carrying out the strategy he sketched at the Hilton, and reviving KKR’s biggest holding. First Data has curbed expenses, reduced debt costs, and improved cash flow. Investors just gave the company a partial vote of confidence: First Data’s IPO, on Oct. 15, was the largest of 2015, raising $2.6 billion and giving the company a market cap of $14 billion. In the wake of the offering, Bisignano, Nuttall, and others on First Data’s team gave Fortune an exclusive account of the company’s turnaround.

It’s a welcome reversal of fortune for KKR. When it took First Data private in 2007, it paid the equivalent of $15.81 a share; after the IPO, shares traded around $16. That’s hardly a return to boast about (the S&P 500 is up 31% since the buyout); but for KKR, which, along with its investors, still owns 60% of the company, the investment has swung from a loss of $2.5 billion to a modest gain. “Frank is proving we were right about First Data’s potential after all,” says Nuttall.

But Bisignano’s view of that potential is wider than anything KKR originally envisioned. He wants First Data to offer ice cream parlors, hairdressers, and every manner of small merchant the high-tech analytical tools that until now have benefited only the likes of Walmart (WMT) and McDonald’s (MCD). “For years, we’ve been selling small businesses these dumb ‘bricks’ that do nothing but swipe cards,” he says, in a gravelly voice—the legacy of a bout with throat cancer. “We’re replacing those bricks with bar and countertop computers that will manage inventory and tell you which waiters at which tables sell the most expensive bottles of wine.” His big idea: Arm new terminals—specifically, First Data’s Clover devices—with business-boosting apps, and customers will reward the company with Apple-like loyalty and the soaring revenue that comes with it.

Bisignano says First Data’s huge customer base—the company manages payments for 6 million merchant locations worldwide—will help him capture enough new business to make a major difference, especially at a time when new regulations are pressuring many businesses to upgrade their equipment. If he’s wrong, First Data may still generate enough revenue from traditional businesses to become modestly profitable again. But if he’s right, it could harness the Clover and its heirs to become one of the top moneymakers in financial services.

You may never have heard of First Data, but chances are it has handled hundreds or even thousands of your credit card transactions. It’s a central pillar in payment services, one of the fastest-growing and least understood industries on the planet. “More and more businesses that used to take only cash, from taxis to dry cleaners, are switching to cards,” notes Tien-tsin Huang, an analyst for J.P. Morgan, and consumer habits are changing accordingly. From 2009 to 2014, credit card, debit card, and electronic payments surged more than 40% in the U.S., to around $6.5 trillion. By 2018 some 81¢ of every dollar spent will be card based or electronic, vs. 65¢ today.

In this $900 billion global business, the best-known players are Visa (V) and MasterCard (MA), but First Data is a quiet giant: Its 2014 revenue of $11.2 billion exceeded those of MasterCard ($9.5 billion) and approached those of Visa ($12.7 billion). It’s the only stalwart operating in all three major fields of payment services, and it dominates two of them.

In “merchant acquiring”—selling credit card terminals to merchants and servicing their accounts—First Data is the biggest competitor. Its 6-million-customer base generates 74 billion transactions a year, or 2,300 a second. First Data is also huge in transaction processing, for both merchants and banks: It checks accounts for fraud, ensures that there’s sufficient cash to cover transactions, approves or declines them, and sends statements on behalf of banks. First Data handles processing for 42% of all card transactions in the U.S., involving hundreds of millions of cards; its blizzard of statements makes it one of the U.S. Postal Service’s biggest customers. All told, First Data processes a staggering $1.7 trillion in payments a year in the U.S., the equivalent of 10% of GDP. (It also has a broad footprint outside the U.S., generating around 25% of revenue overseas.) In a third business—coordinating transactions data among merchants, processors, and banks—First Data’s STAR debit network is a smaller presence; nonetheless, First Data often receives revenue from three sides of a transaction: from the merchant, from the bank, and through STAR.

In short, First Data runs the kind of invisible-but-essential business on which Bisignano built his reputation. A Brooklyn-born grandson of Italian immigrants, he’s spent most of his career building or fixing back-office operations at major banks. His 29th-floor, glass-walled office overlooking the 9/11 Memorial Plaza shows how far such work has taken him. On the walls hang photos of Bisignano grinning with a gallery of the powerful and famous, from Timothy Cardinal Dolan of New York to Arizona Cardinals star Larry Fitzgerald. Above all, he prizes a portrait of the J.P. Morgan Chase (JPM) management team from 2008, featuring him with former boss Jamie Dimon and two other alumni who now lead huge financial companies—Bill Winters, chief executive at Standard Chartered, and Charlie Scharf, CEO of Visa. Also in the photo: Jes Staley, the front-runner to become Barclay’s new chief executive, and former Citigroup CFO Heidi Miller, now a First Data director.

In 1994, Dimon hired Bisignano to run operations at Smith Barney. As Dimon and Sandy Weill made acquisition after acquisition, culminating in the purchase of Citicorp in 1998, Bisignano’s roles in everything from IT to purchasing steadily grew. By 2001, Citi had 16,000 staffers in downtown Manhattan, many working for Bisignano. On the morning of Sept. 11, after the first World Trade Center tower fell, Bisignano rushed to the street, megaphone in hand, and yelled, “Walk north!” He then led thousands of Citi workers to safety at an operations hub on West 34th Street, and later kept Citi’s computers running amid the post-attack chaos.

Bisignano also proved that he could revive underperformers. In 2002 he took over Citigroup’s Global Transaction Services, a money-losing backwater; he reinvented it as a center where multinationals could outsource accounting and foreign-exchange transactions, and by 2005 it was generating more than $1 billion in annual profit. In late 2005, Dimon lured Bisignano away from Citigroup to be chief administrative officer at J.P. Morgan Chase; there he turned around a mortgage business encompassing the foreclosure-laden portfolio of the former Washington Mutual. (Bisignano accomplished that after his fight with throat cancer, a condition that he speculates may have come from working in toxic soot after 9/11.)

In 2012, Dimon promoted Bisignano to co-COO. But Bisignano felt ready for a top job. “All my mentors, like Sandy Weill and Jim Robinson [ex-CEO of American Express] said it was time,” says Bisignano. One Thursday in 2013, Nuttall says, he heard from old Citi friends of Bisignano’s (including Joe Plumeri, who’d gone on to run an insurer for KKR), confiding that “A little birdie says Frank might be willing to make a move.” Two days later, Bisignano and Nuttall were face-to-face at the Hilton.

There were plenty of problems on the menu. KKR’s buyout had burdened First Data with $22.6 billion in debt, at extremely high interest rates. “The thesis was that First Data would innovate and keep growing,” says Nuttall, “so as cash flow would keep rising, we’d pay down the debt,” reaping outsize returns as equity expanded. But the deal closed in September 2007—just before the Great Recession, when credit and debit card transactions dropped sharply. Beginning in 2010, First Data’s revenue stopped growing for the first time ever; cash flow plummeted too. And First Data’s processing services were becoming commoditized: Each year, Nuttall says, the company lost about 15% of its merchant customers to competitors that offered lower fees and better service.

First Data’s troubles had already thwarted two accomplished CEOs—former Compaq and WorldCom chief Michael Capellas (2007–10) and ex-Paychex CEO Jon Judge (2010–13). By the time Bisignano arrived, KKR had put two of First Data’s major businesses up for sale, the STAR debit card network (now a leader in PIN-less debit transactions) and its private-label credit card franchise. Bisignano called off both sales: For him, retreat wasn’t an option. He reasoned that if First Data could escape the commodity syndrome by following his iPhone vision, it could become highly profitable.

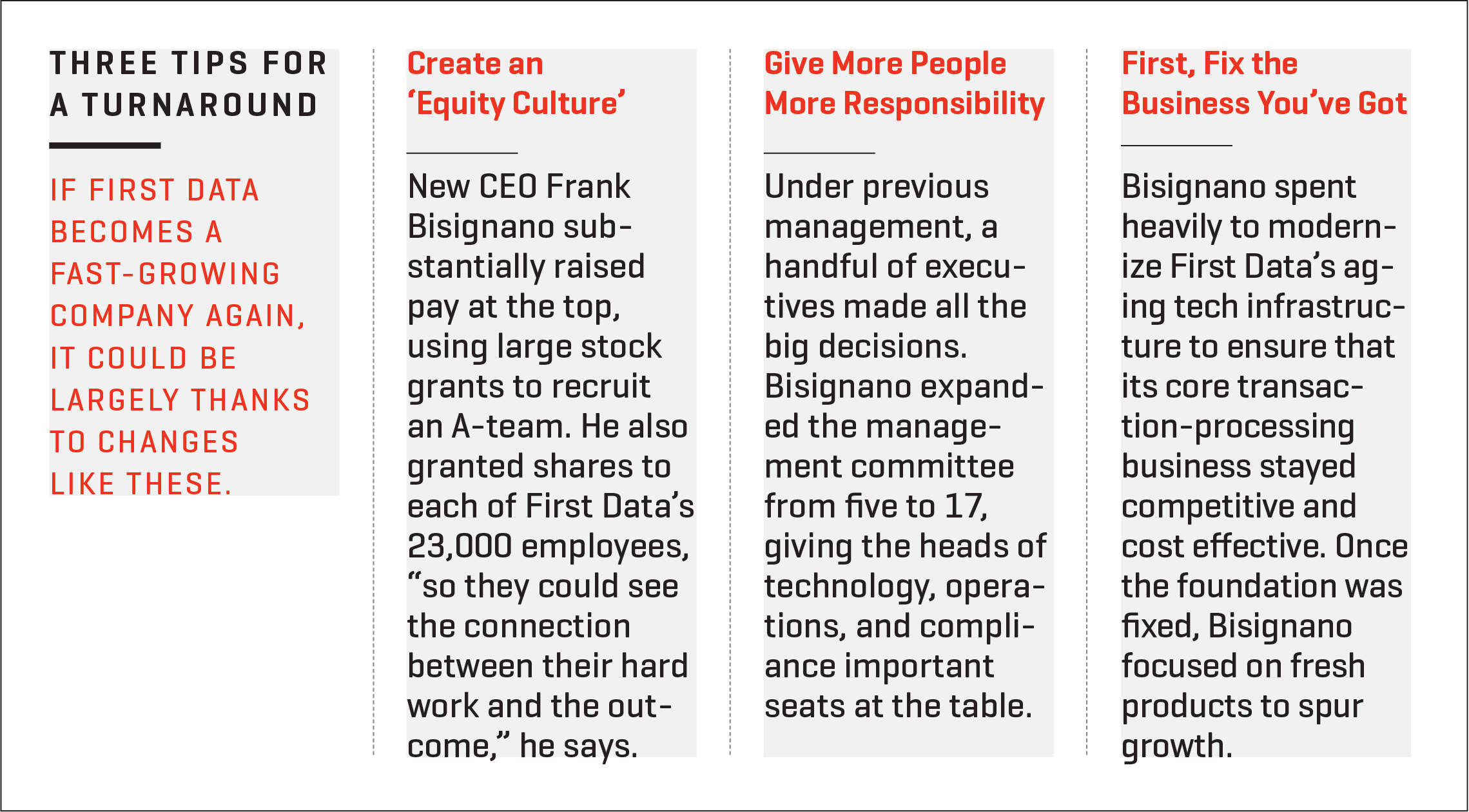

First the company needed a fresh culture. Prior to Bisignano’s arrival, a small group of executives had handed down orders to its 23,000 employees, and neither technology nor operations had a seat on the management committee. “Five guys were running the company,” he recalls. Visiting headquarters in Atlanta, he saw “these palatial offices far away from everyone else, including a suite for the CEO with a sitting room and bathroom.”

Bisignano ripped out the offices, replacing them with 200 workstations. He also expanded the management team, giving more people broader responsibilities. Just as his mentor Dimon had drawn loyalists from Citigroup to J.P. Morgan, Bisignano recruited lieutenants from among his former J.P. Morgan and Citi (C) collaborators, including his president, Guy Chiarello; compliance chief Cindy Armine-Klein; operations head Christine Larsen; and CFO Himanshu Patel. (Plumeri became vice chairman.) Bisignano also moved First Data’s executive offices to New York City, although headquarters remain in Atlanta.

To attract talent, First Data enormously increased compensation at the top: Annual pay packages in the $7 million to $10 million range, mostly in stock, are now the norm for the management committee. The boss himself is reaping royal rewards. In 2013 and 2014, Bisignano received stock and option grants valued at $77 million; after the IPO, by Fortune’s estimates, his holdings are worth well over $100 million. Bisignano also insisted on making every rank-and-file employee a shareholder. “I told KKR, ‘I’m going to ask a lot of people to do a lot of hard things,’ ” he says. “They should see the connection between their hard work and the outcome.” As his mentor Weill tells Fortune, one strength of Bisignano’s is that “he can relate down as well as relating up. CEOs who can’t relate down get in a lot of trouble.” All told, First Data has issued about 2.2% of its shares, worth some $300 million, to its employees.

Bisignano’s team has frozen operating expenses—in part by flexing its tech muscles. First Data had been assembled from multiple acquisitions and hadn’t integrated its crazy quilt of some three dozen separate platforms. Systems for gas stations, restaurants, and clothing stores, for example, operated on totally different software. In its first eight months, the new team spent $180 million to replace outdated servers and storage and began shrinking the number of platforms. “We threw out 60 tons of old equipment,” says Chiarello—an amount greater than the weight of a Boeing 737, he points out.

Bisignano and KKR are also attacking First Data’s interest burden. A $3.5 billion private placement in 2014 went mainly to lowering debt. Over the past 16 months, they’ve refinanced about $8 billion in borrowings—including $2.1 billion in fixed-rate loans, on which they trimmed the average interest rate from 7.75% to 4.9%. The result: a $300 million reduction in annual interest payments, to $1.6 billion. As Wedbush’s Luria points out, the debt remains a major drag: About half of First Data’s remaining debt is pegged to variable rates, so the company will face higher expenses if rates climb. Indeed, First Data’s IPO priced lower than many commentators expected, reflecting investors’ concerns over the debt load. Still, proceeds from the offering could lower First Data’s debt to $18.5 billion, taking the company closer to sustained profitability.

Even as it brought costs in check, Bisignano’s team searched for products that could lure more merchant customers by improving on the old bricks—and the team viewed small businesses as the biggest opportunity. Large retail chains, from McDonald’s to Macy’s, benefit from sophisticated point-of-sale systems equipped with special software for managing inventory, employee schedules, and other functions. But although small businesses account for 70% of U.S. transaction-management revenue, data-analysis innovations and management tools for those merchants lagged far behind. “They were stuck with the same old technology for at least 15 years,” says Chiarello.

Bisignano aims to replace those bricks with app-rich new devices. And while persuading customers to change might otherwise be onerous, First Data has timing on its side. On Oct. 1, a new rule took effect that will press merchants to buy new “dip” terminals designed to read EMV cards, which are equipped with a microchip to prevent fraud. Until now, card issuers have been liable when thieves use information from a credit or debit card’s magnetic strip to make fraudulent charges. EMV cards have a strip and a chip; going forward, if a merchant doesn’t have a terminal that can read the chip and thieves use an EMV card’s strip data, the merchant, not the issuer, will be liable.

As “reterminalization” kicks in, First Data hopes to scoop up customers with the EMV-friendly Clover. (“It’s our daily bread,” says Bisignano.) Clover is the product of a Silicon Valley startup First Data bought before Bisignano arrived, but his team recognized its potential as a platform for merchant-ready apps. Clover comes in four versions: The Station, a large screen mounted above a cash drawer, debuted in 2013, and over the past year First Data has added the handheld Mobile; the Mini, which can fit on a countertop; and the Go, a card reader that plugs into a cellphone.

As First Data encourages developers to build apps for Clover, its size has proved to be a strength. Smartphone app makers, Bisignano notes, “want to go with an Android or iPhone, the platforms with the biggest markets”; First Data’s omnipresence gives Clover similar clout. The company says Clover has attracted more original features than any other small-business terminal: 106 so far, with 277 more in the works. The Salon Scheduler app reminds spa and manicurist clients of appointments and prompts them to rebook if they’ve been absent. Give an app called Stock the data on how much sauce and cheese goes into a large pizza, and it will reorder ingredients automatically, based on your sales.

The most popular app is an employee-management tool called Homebase. It’s been a boon to Angelo Vivolo, proprietor of Vivolo, an Italian eatery on Manhattan’s Upper East Side. “I can check how much revenue each waiter generates every night,” he says. “If a waiter is getting low tips, there’s a good chance they’re providing bad service.” Servers check in for work by typing in a PIN, and a tiny camera takes their picture to ensure no one is faking. The Clover, says Vivolo, gives him tools that big businesses already have. “It’s like going from the Stone Age to the modern era,” he says.

First Data’s hope is that apps like these will persuade customers to shun rival processors, even if they’re cheaper. The apps could also greatly enhance the revenue First Data collects from each customer. Take the example of a pizzeria generating $200,000 in annual sales. Currently, First Data’s share of its account management, processing, and transaction fees would total about $2,000 a year. If the pizza maker upgraded to the Clover and used its various apps and services, First Data could reap another $60 to $100 a month in fees—a bump of as much as 60% over the old “brick.” And that’s mainly profit: With its huge computing infrastructure already in place, the extra services generate little additional cost for First Data.

First Data is also exploiting big data. For years the company didn’t save the enormous quantities of information it collected. Bisignano put a stop to that “gigantic mistake.” And in 2014, First Data teamed up with the Silicon Valley data-analysis specialist Palantir Technologies to develop a new First Data product called Insightics, which deploys the processor’s vast store of information to provide consumer-research tools to small businesses like Tin Pot Creamery.

Becky Sunseri, a former pastry chef at Facebook, opened that gourmet ice cream purveyor in Palo Alto in 2013, offering such exotic flavors as salted butterscotch, and coffee with cocoa-nib toffee. She was considering a second location, in nearby Los Altos, but she feared that a new shop would cannibalize customers and sales from the original. Sunseri’s Clover rep signed her up for a trial run with Insightics, which costs the typical retailer about $30 a month. Insightics produced a heat map showing where her current customers were coming from. The welcome revelation, says Sunseri: “Only about 1% of them came from Los Altos.” Last November she launched a second location there, and both have thrived. Insightics also alerted Sunseri that Tin Pot’s sales were lowest at midday, so she started offering lunchtime discounts that sweetened sales. From Clover, she says, Tin Pot got “data we would never have the time or the finances to collect or analyze ourselves.”

More than 100,000 Clovers are now in service, even though three of its four models are still new to the market. Larry Berlin of tech research firm First Analysis calls Clover’s sales “okay but not great,” given all the competition in the field. But Berlin goes on to note of First Data, “They have far better distribution than anybody else, which gives them a leg up.”

That’s Bisignano’s belief too. The CEO admits that most Clover sales have gone to new customers, not the merchants First Data currently serves. The company needs to convert hundreds of thousands, if not millions, of its legacy users to become the raging success Bisignano promises. First Data, originally prized by KKR for its boring predictability, may seem like the unlikeliest of contenders for such an accomplishment. But whatever happens with Clover, it’s clear Bisignano has changed the culture of a company once tarred as “too big to succeed.”

A version of this article appears in the November 1, 2015 issue of Fortune with the headline “First Data’s counter attack.”