It’s been a pretty miserable couple of weeks for the U.S. economy.

Last week, the Commerce Department announced that GDP growth in the first quarter of 2015 fell dramatically to 0.2% on an annualized basis. But after new data released Tuesday showed that the trade deficit in March was far higher than economists had expected, it’s likely that GDP in the first quarter actually shrank.

For now, most economists expect that the economy will bounce back in the second quarter of 2015, just like it did last year, and that overall real growth will beat last year’s performance of 2.4%.

But a new analysis from Jodi Gunzberg, global head of commodities at S&P Dow Jones Indices, argues against this consensus, and instead makes the case that we’re headed for another recession.

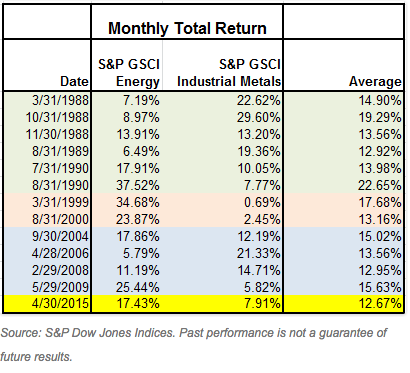

Gunzberg points to the outstanding performance of commodities in April as measured by the S&P GSCI index, which gained 11.1% that month, the 19th best month since the index first starting tracking these commodities back in 1970. Two groups of commodities–energy and industrial metals–did particularly well, rising by a combined 12.67% in April. It’s not common for these two groups of commodities to surge in value at the same time. According to Gunzberg, the two indices have only moved in tandem about 30% of the time since 1983. And there have only been 12 months in which the energy and industrial metals sectors have risen more than they did in April:

As you can see, the months in which these sectors did well are clustered around times leading up to a recession. Gunzberg argues that this is because firms that rely on these materials—like oil and natural gas in the energy sector, and copper and aluminum in the metals sector—start buying up these materials in bulk when they sense their performance is about to start waning. “When you look at broad economic cycles,” says Gunzberg “equities lead the cycle, while commodities are on the cycle.”

In other words, as the market nears a top, and companies are flush with cash and capital, but short on faith in their future performance, they start to hoard the basic commodities that power the global economy. But eventually their performance takes a turn for the worse, and so does demand for raw materials.

Of course, Gunzberg’s data goes back by just 30 years, and it predicts only three recessions. It’s possible that these data only point to strange coincidences rather than something with real predictive power. But with the U.S. in its 70th month of economic expansion–the sixth longest the U.S. economy has had since 1850–the slowdown in the first quarter may very well be more than just a blip.