THE OPTIMISM IS BEAMING like the summer sun. America’s big-company CEOs are bursting with confidence, in June expecting to take in even more revenue and make bigger investments than they foresaw in March, when they were more confident than ever before in the 15 years the Business Roundtable has been surveying them. CFOs are just as ebullient. Their perception of the North American economy was recently the highest in the eight years Deloitte had been asking about it. Leaders of small businesses also are brimming with optimism—more than at any time in the past 30 years, reports the National Federation of Independent Business. At least figuratively, confetti is flying, disco balls are spinning, and Champagne corks are popping across the length and breadth of American business.

It seems a shame to pull the plug on the dance music, so we won’t, exactly. As of mid-July, forecasters were expecting the announcement of a knockout GDP growth number for the second quarter, and it wouldn’t be surprising if the U.S. economy continued to grow impressively for at least a few quarters more. Unemployment is near historic lows, and better job prospects are drawing more workers back into the labor force. No wonder business leaders are confident.

Yet all these signs of economic strength mask fundamental realities that won’t fade away and mustn’t be ignored. The current economic expansion is much nearer its end than its beginning, as accumulating hints suggest—including the stagnating stock market, about which we’ll say more in a bit. Already the concerns are pushing up long-term interest rates, which is bad for asset values. Uncertainty about the effects of a trade war is causing many companies to postpone action, dampening potential investment. Indeed, look past those disco balls and you’ll see economic warning signs everywhere. A significant slowdown or even recession is coming sooner or later, and it’s probably coming sooner than you think. It always does.

A Seasonal Change is Coming

LET’S START WITH THE OBVIOUS: Economies follow cycles. Unlike with seasons or the moon or the ocean tides, the timing of the business cycle is never easy to predict. But at some point, economic activity reaches a temporal peak, then begins to contract until eventually it bottoms out and starts growing once more. A familiar sign that we’re in the waning stage of the growing season, ironically, is that the economy overheats—think of it as an Indian summer: Companies push factories to produce more than their long-term sustainable output, pushing employees to work more overtime. Demand is so strong that inflation starts to increase, leading central bankers to raise interest rates, which causes asset values, including stock prices, to level off or fall. Ray Dalio, CEO of the world’s largest hedge fund, Bridgewater Associates, writes, “That is why it is not unusual to see strong economies accompanied by falling stock and other asset prices.”

All of that is happening now. The Congressional Budget Office finds that this year, the economy has begun overheating in just this way, producing more than its sustainable longterm potential. The CBO predicted in May that as wages rose, more people who had left the labor force would come back to work, and, yes, that’s just what happened in June. The labor market continues to be tight, with workers so confident that they’re voluntarily quitting their jobs at the highest rate in 17 years. Meanwhile, employers will likely have to bid up wages in order to attract and keep good workers, hitting corporate earnings directly.

Inflation and interest rates are rising and will likely continue to do so, forecasts the CBO. With all those factors combining, says Dalio, “We know that we are in the ‘late-cycle’ part” of the business cycle.

“It is not unusual to see strong economies accompanied by falling stock and other asset prices… we know that we are in the ‘late-cycle.'”

Ray Dalio, CEO, Bridgewater Associates

It is somewhat remarkable, historically speaking, that it has taken this long to get here. America’s current expansion is 110 months old (including the recovery period after the last recession), which makes it a marvel of longevity—the economic equivalent of a supercentenarian. The current growth run is the second longest in the 164 years for which the National Bureau of Economic Research has done the analysis; the average expansion has run a mere 39 months. The only one that outlasted this one lived to be 120 months old (1991–2001).

Old age isn’t by necessity a death knell for an expansion—but then, there is something that tends to accompany it: When things start to break down, they break down en masse. Gerontologists call these tandem and often interlinked pathologies “comorbidities.” And in this economy, just under the skin, there seem to be plenty of them.

We Don’t Have Enough Workers

ECONOMIC OUTPUT is pretty straightforward in concept: It’s a function of labor, capital, and productivity. The simple fact is, it’s hard for an economy to grow very fast if the labor force is growing very slowly, as the U.S. labor force is doing. In the 1970s, it increased at a 2.6% annual rate; now the rate is about 0.2%. One reason for this is that for many decades, Americans have been having fewer and fewer babies (the U.S. fertility rate dropped to a new all-time low last year). As the baby-boom generation continues to age and exit the workforce, the number of American-born workers will sharply decline. This past October, the Bureau of Labor Statistics projected that over the period of 2016 to 2026, there will be 11. 5 million jobs created and a million fewer people in the workforce to fill them.

To counter that demographic drag, American companies have relied on an influx of people from outside the country. Immigrants accounted for 17.1% of the U.S. workforce in 2017, a percentage that has been rising for years. This critical labor force infusion, in fact, has been “as close to a free lunch as there is for America,” as Neel Kashkari, president of the Federal Reserve Bank of Minneapolis, put it earlier this year in an op-ed for the Wall Street Journal.

What’s less widely understood is that there has actually been a global competition for this supplementary workforce. That’s right: Other developed nations with declining birthrates likewise need new workers to help offset their armies of retirees—and America has been winning this battle, luring not just low-wage workers to fill jobs that native-born Americans aren’t rushing to do but also scientists and entrepreneurs. (Witness the Silicon Valley billboards, bought by the government of America’s northern neighbor, imploring techies with visa troubles to “Pivot to Canada.”) That’s why President Trump’s immigrant-hostile policy isn’t just a political stance, it’s also an economic one—and one that’s almost sure to limit the ability of U.S. companies to grow.

So far, America’s immigration crackdown has not significantly reduced net in-migration, but it’s a compounding risk that could have far-reaching consequences for American businesses large and small.

A Trade War Makes Other Problems Worse

BY ITSELF, the Trump administration’s immigration policies may not be enough to stop growth in its tracks. But another federal policy is making even more trouble at the border—this time with America’s long-standing trading partners. Nascent trade wars with China, Europe, Canada, and Mexico—even if they don’t last—have become yet another comorbidity for our aging expansion. U.S. companies that do most of their business abroad grew faster and were more profitable than the rest last year, just as in previous years, FactSet reports. Waging a trade war thus disproportionately hurts America’s strongest engines of economic growth.

By the numbers, the trade-related skirmishes so far are insignificant in America’s $20 trillion-a-year economy. Even the tit-for-tat imposition of tariffs on $34 billion of trade by the U.S. and China in early July will not, by itself, noticeably reduce GDP. Yet the effects could easily mushroom, in two intertwined ways.

First, even the biggest wars typically start with minor battles that spark an unstoppable cycle of escalation. In the current trade war, that appears to be underway. Hostilities with China began in March when President Trump imposed tariffs on aluminum and steel imports, only about $2.7 billion of which come from Chinese producers. China responded with new tariffs on an equivalent amount of U.S. exports. The next day, Trump proposed tariffs on $50 billion of Chinese imports; China proposed retaliatory tariffs the day after that. On and on this went until the U.S. has now threatened tariffs on nearly all of America’s $500 billion of Chinese imports, and China has vowed to retaliate “at any cost.”

Economic stimulus “is going to hit the economy in a big way this year and next year, and then, in 2020. Wile.e Coyote is going to go off the cliff.”

Ben Bernanke, Former Federal Reserve chairman

As the stakes get higher, the rhetoric gets more bellicose. China is “threatening United States companies, workers, and farmers who have done nothing wrong,” Trump said in June. China’s Trade Ministry called the speech “blackmail.” When the latest tariffs took effect in July, a Chinese Communist Party newspaper warned that “Washington has obviously underestimated the giant force that the world’s opposition and China’s retaliation can produce.”

As public threats become more explicit, backing down from them appears ever less likely. That’s how a piddling spat between the world’s two largest economies, jointly the foundation of global economic growth, could become a historic trade war.

But the second way the current dispute could damage the U.S. economy doesn’t even require that hostilities get worse. It requires only that people become less certain about where all this is headed. That effect—an “uncertainty shock,” as Bank of America Merrill Lynch economist Michelle Meyer called it in a recent note—is happening already, and it worries the Fed. “Contacts in some Districts indicated that plans for capital spending had been scaled back or postponed as a result of uncertainty over trade policy,” the Federal Open Market Committee reported from its June meeting, adding that “most participants” were concerned such uncertainty could depress “business sentiment”—confidence, that is—“and investment spending.”

Don’t expect much more clarity anytime soon. No one can predict where a large-scale trade war would lead. The last one occurred in the 1930s, when today’s intricate, light-speed global supply chains would have been nearly unfathomable. Which leaves business decisionmakers only to wonder how all this shakes out.

Uncertainty prompts paralysis—and that’s no good for growth.

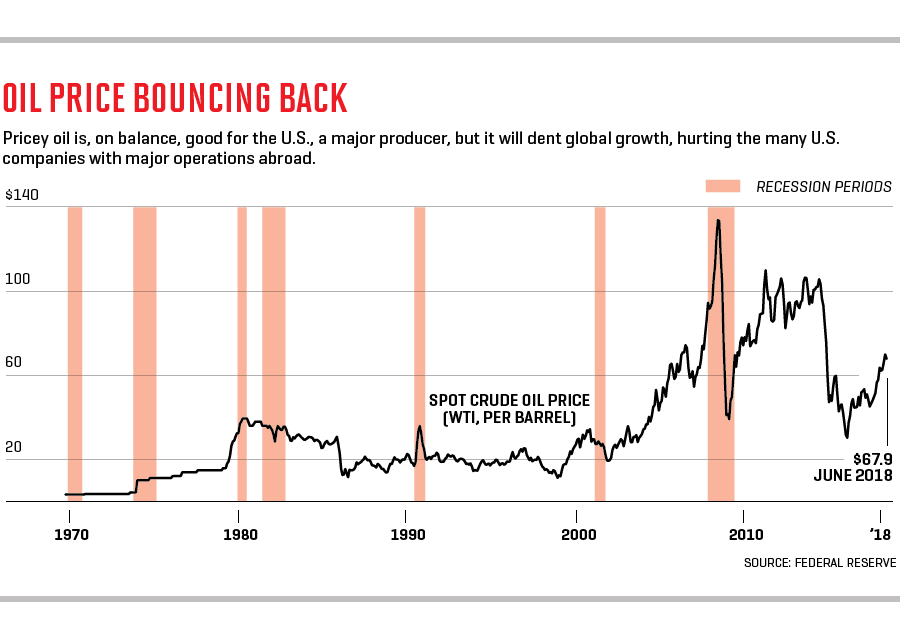

Rising Oil Prices Will Gum Up Global Gears

ANOTHER THREAT—this one lingering just below the top news headlines—is the high price of oil. Recently around $73 a barrel, it’s on balance a direct benefit to the U.S. now that America is a prodigious producer of the fossil fuel—but expensive oil is also very likely to dent global growth, particularly since the strengthening dollar makes oil (wherever produced) yet more costly for other countries.

The Organization for Economic Cooperation and Development, an intergovernmental agency aimed at fostering economic growth worldwide, points to high oil prices as one of the main “risks that loom large.” And while a broad global slowdown may seem, to some, removed from U.S. interests, it would hurt America’s biggest companies and many of its smaller ones as well.

The Stimulus May Pad Growth For A While…

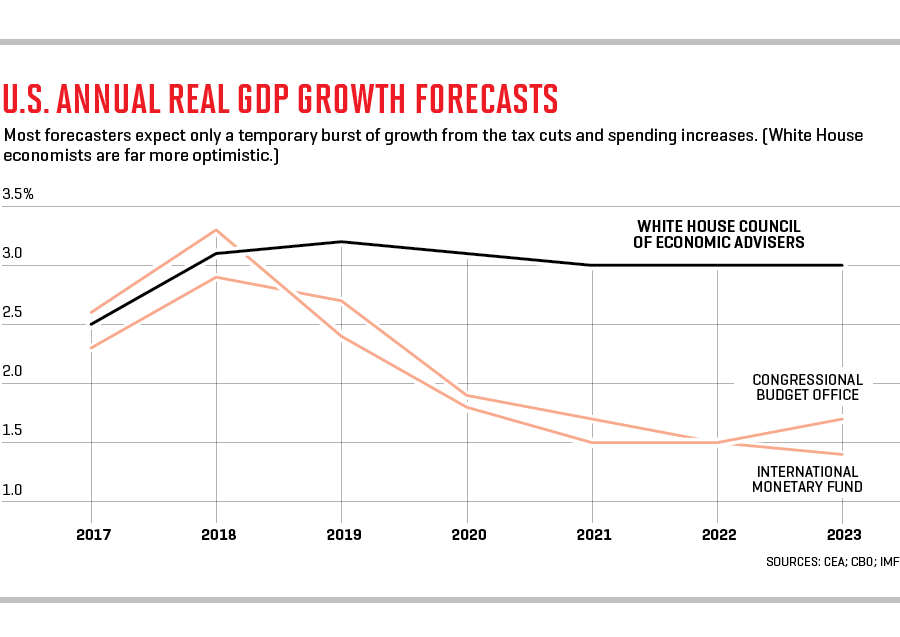

THE SIGNS of economic senescence and stress, as we noted, would seem to mirror the end of past business cycles. But there’s one big counterpoint, as we’ve all heard many a time, and that’s the recent federal tax cut and spending increases. That whammy of a stimulus, say some economists, will stave off any recession—and not only that, it will jumpstart growth for years to come.

Indeed, the economy, by all traditional measures, seems to be growing smartly. After years of low-horsepower expansion, 2018 could be the best year for GDP growth in at least a decade. But don’t count on the stimulus to keep stimulating.

Robert J. Gordon, the Northwestern University economist whose latest book is The Rise and Fall of American Growth, argues persuasively that America’s “special century” from 1870 to 1970 represented “a singular interval of rapid growth that will not be repeated.” Regular yearly GDP growth of 3%, once considered normal, is no longer sustainable, he says. Yet “old-fashioned fiscal stimulus” from tax cuts and a spending boost will produce a brief but powerful blast of growth—“3%-plus growth for at least a while” and “an average of 3% growth probably for the next four to six quarters.” Then, he says, “the stimulus fades away.” And it’s back to the slow-growth new normal.

That, of course, assumes we’ll get that short-term boost. We may not. The stimulus may not work as advertised for a number of reasons. First, fiscal fire-starters like tax cuts and spending increases are usually deployed at the bottom of the business cycle, not the top. They just don’t add much oomph to an economy that’s already growing, say researchers at the San Francisco Fed in a new study. The evidence suggests that “the true boost is likely to be well below” what many forecasters predict and could be “as small as zero.”

Former Fed chairman Ben Bernanke foresees a more dramatic near future. The stimulus is arriving “at the very wrong moment,” he said at a recent Washington policy discussion. (He declined an interview request.) “The economy is already at full employment.” The stimulus “is going to hit the economy in a big way this year and next year, and then, in 2020, Wile E. Coyote is going to go off the cliff.”

What’s more, many companies are spending their tax bonus on share buybacks rather than investing it in operations. That may make shareholders happy for a while, but it’s not going to stimulate economic growth over the long haul. Our take is that while the stimulus might extend this expansion, it’s a lot like flooring the accelerator in a car. For a time, you go really fast, and it might even be thrilling—but pretty soon you run out of gas … or crash.

…And Then It May Make Things Worse

THE STIMULUS, it’s important to note, will have another effect as well: The accumulated federal deficit over the next decade will be $1.6 trillion larger than it would have been without the recent tax cuts and spending increases, according to the CBO—and it will be larger still if various tax and spending provisions set to end are renewed by Congress, as seems highly likely. That’s concerning for all kinds of reasons (as Fortune’s Shawn Tully showed in “Deep in Debt,” April 1, 2018). When the next recession inevitably arrives, Washington will be less able to apply the usual remedies of lower taxes and greater spending. If ballooning debt eventually spooks foreign investors into buying fewer Treasuries, rates will have to rise and federal interest payments will grow, expanding the debt even faster in a bad-news feedback loop.

Many Companies Are Already Overleveraged

WHILE MUCH has been said about the growing menace of federal debt, trouble is brewing as well in a different and largely overlooked credit risk: corporate debt. Without many alarm bells sounding, the debt of nonfinancial companies has risen to 73.5% of GDP—an all-time high.

It hasn’t been a problem so far because interest rates have been so low—which is a big reason companies borrowed so heavily in the first place. But as interest rates rise, the Goldilocks environment is darkening. Today’s record corporate debt “would be a problem if rates are rising while the economy slows—a double whammy,” says S&P Global credit analyst Andrew Chang. That’s exactly the scenario that is beginning to seem more likely. “People are aware of the risk but not quite behaving like an aware citizen,” he tells Fortune. Investors in corporate bonds are getting nervous. Investment-grade corporate debt was the worst-performing category of debt investment in this year’s first half.

Some debt holders try to comfort themselves by noting that U.S. corporations are sitting on nearly $2 trillion of cash. But that reasoning faces two big holes. First, just 24 companies account for about half of that mammoth cash cache (led by Apple, with $267 billion), yet they account for nowhere near half of America’s corporate debt.

Second, corporate America’s net debt—that is, debt minus cash—is still about 1.5 times Ebitda (earnings stripped away from interest, taxes, depreciation, and amortization). That would make it the highest debt-to-earnings ratio in the past 15 years. “Cash may be at an all-time high, but so is debt,” says S&P Global’s Chang, “and people aren’t noticing the second part.”

The situation is serious enough to grab the Fed’s attention. Fed governor Lael Brainard, speaking in April, said, “Our scan of financial vulnerabilities suggests elevated risks in two areas: asset valuations and business leverage.” Both risks involve corporate debt. Brainard noted that yields on corporate bonds are “low by historical comparison,” meaning the bonds look awfully expensive. And business leverage, like that debt-to-earnings ratio, is “high relative to historical trends.”

Got all that? Well, if not, maybe this comment from the Treasury’s Office of Financial Research—the arm of the department that assesses U.S. financial stability—can bring home the message: “Nonfinancial business leverage ratios … are flashing red on the heat map” of potential vulnerabilities.

Those trends trouble central bankers because all it takes is a single jolt, in some cases, to create a cascade of corporate havoc. As Brainard observed, “unexpected negative shocks to earnings in combination with increased interest rates” could hammer those bonds and the lenders who own them. If that happens, it won’t just stress the bond market. The effects could ripple through the whole economy.

Reliable Indicators Are Pointing Down

FOCUSING ON DEBT and its cost is wise because bond interest rates boast an excellent record of forecasting recessions—and they’re close to predicting one now. When the yield on long-term (10-year) Treasury securities falls below the yield on short-term (threemonth) Treasuries—an inversion of the yield curve—a recession is on the way. Over the past 50 years, this test has given no false positives or failed to signal a coming downturn. Yield curve inversion has always equaled recession, and the only question is how long it will be before the recession starts; on average, it’s 10 months, though it took 16 months before the 2008–09 recession.

As of mid-July, the yield curve had not inverted, but it was getting close—closer than it has been since just before the 2008 financial crisis and recession, according to Haver Analytics.

Another highly reliable presage of downturns is surprising. It’s a trough in the unemployment rate—counterintuitive because low unemployment shows that an economy is growing strongly. But super-low unemployment also means the expansion is pressing up against its limits. In the past 65 years, this indicator has never missed and has never called a false positive.

Complicating such a call is the fact that we can’t be sure a trough has occurred until after the fact. Unemployment hit a 17-year low of 3.8% in May, then edged up to 4% in June as more workers rejoined the labor force looking for jobs. Whether that turns out to be a bottom won’t be known for at least a few more months. For now, though, we can only say it’s hard to believe we aren’t at least very near one.

When the markets and the economy inevitably do turn, it will be, like all change, an opportunity.

In addition to knowing which indicators are best at predicting recessions, we also know whom not to ask: economists. At least on this one task, they’re terrible. Around the world, over long periods of time, the consensus of economists has consistently failed to predict recessions even a few months before they begin. Ned Davis Research finds that in the U.S., “economists, as a consensus, called exactly none” of the seven recessions since 1970. In fact, economists typically do not “forecast” a recession until after it has started, and even then they initially understate the decline, revising their estimates until finally getting them right shortly before the recession ends. Economists are highly valuable in helping the rest of us understand how the economy works, but they’re notably reluctant to predict downturns.

This is important to remember because it means the experts won’t tell us a recession is coming until it’s already here. Which means it’s up to you to prepare for it. (For some help, see the sidebar “Where to Invest When the Party Ends” on the next page.)

Analysts Are In Fantasyland

AGAINST THAT BACKDROP, Wall Street analysts seem utterly clueless in their optimism. Consider that over the past 70 years, U.S. corporate profits have grown at a 5.6% compound annual rate. During the greatest bull market in history, from 1982 to 2000, they grew at 6.5%. Yet Wall Street analysts believe the profits of the S&P 500 companies will rage ahead at a searing 15% annual pace—not for a few quarters, but over the next five years.

One of the all-time great investors, John Templeton, said, “Bull markets are born on pessimism, grow on skepticism, mature on optimism, and die on euphoria.” This sounds like euphoria, or what we might less politely term insanity.

Trying to call turns in the market is folly, and there’s no telling how stocks might perform in the next six or 12 months. Even if today’s prices are in fact far too high, the market need not plunge. It could just stagnate until profits eventually catch up with prices.

Two of the best investors alive think there’s even a chance of a brief market leap before sanity returns. Ray Dalio is watching for “one last spurt in equities prices,” which he considers a key element of “the classic top.” Fund manager Jeremy Grantham, who spotted the dotcom and housing bubbles well in advance, calls it a “melt-up,” a final, rapturous delirium of buying that signals a bull market’s decisive end. See the last three months of 1999 for a dramatic example.

Exactly how and when a bull market will expire is unknowable, but signs are piling up that this bull market, now in its 10th year, has about run its course. Dalio and other sophisticated investors say they can’t find stocks worth buying. CNBC’s latest Millionaires Survey reveals that rich investors are moving out of stocks and into cash or near-cash investments. Nobel Prize–winning economist Robert Shiller of Yale regularly surveys investors on their confidence that stocks are not overvalued; the latest reading is the lowest since 1999.

Yet those Wall Street analysts are having none of it. “It’s kind of like we’re in 1928 at the moment,” says Shiller. “There’s still all this optimism and a sense that it would be unpatriotic to disturb it.”

So Don’t Just Beware, Prepare

FROTHY STOCKS, economic indicators pointing down, financial stability flashing red, trade war, and more—it’s a lot to worry about. It doesn’t necessarily mean calamity is just ahead. For all we know, stocks could resume rising or even “melt up,” as Grantham says. The economy may well grow impressively this year. But we don’t have to look much further out to get more nervous. No one except the Council of Economic Advisers seems to think GDP can grow at 3% over the long term, and if the recent stimulus turbocharges growth, it does so at a price that will have to be paid afterward. The economic cycle hasn’t been abolished; all evidence says we’re in the latter stages of one. And we had better be ready for the next recession, because when it arrives, economists will not have predicted it.

When the markets and the economy inevitably do turn, it will be, like all change, an opportunity. Stocks will be on sale, and corporate managers should remember that the competitive order in any industry always changes more in adversity than in smooth sailing.

Clearheaded investors and leaders come through downturns fine because they confront reality early—and in the best of times, they prepare for the worst.

A version of this article appears in the August 1, 2018 issue of Fortune with the headline “The End is Near.”