Even before the New York Attorney General revealed a bombshell lawsuit last week against Bitfinex and Tether, you probably had some concerns.

Suspicion has swirled around Bitfinex and Tether, which share the same owners and management, since at least early 2018, most of it focused on whether Tether, a stablecoin backed by the U.S. dollar, really holds a dollar in reserve for each coin.

The controversy intensified in the middle of last year after researchers from the University of Texas at Austin found that sales of Tether seemed to have been used to pump the price of Bitcoin during its run-up in 2017, suggesting that Bitfinex may have used the stablecoin to manipulate the market. (As a reminder, Tether has become an increasingly important player in the cryptocurrency markets, accounting for more Bitcoin trading volume than even the dollar.)

And yet, the problems detailed in the NYAG’s lawsuit go beyond what most people suspected. And they center around a Panama-based payments processor called Crypto Capital Corp. Last year, the court filings allege, Bitfinex handed over more than $1 billion to Crypto Capital in order to process client withdrawal requests, without so much as a piece of paper specifying terms of the deal:

Despite the sheer amount of money it handed over, Bitfinex never signed a contract or other agreement with Crypto Capital. In mid-to-late 2018, executives at Bitfinex/Tether began to suspect that Crypto Capital had lost, stolen, or absconded with the funds, and as of today, the companies have been unable to locate, much less recover, approximately $850 million dollars handed over to Crypto Capital. None of that has been disclosed to investors.

If you’ve been following the events in the cryptocurrency world that we’ve covered in this newsletter, the saga may remind you of another recent case of lost or stolen money—QuadrigaCX, the Canadian cryptocurrency exchange which said earlier this year that it lost access to $190 million in funds following the death of its CEO.

As it happens, both Bitfinex and Quadriga used the same Panamanian payments processor: Crypto Capital. In fact, Crypto Capital still lists Quadriga as one of its clients on its website. And as we learned on this week’s episode of “Balancing the Ledger,” which you can watch below, there’s evidence that payments clients made to Quadriga may never have arrived at all.

Bitfinex, for its part, is denying any theft by the third-party processor, but also raising more questions, writing in a statement Friday, “On the contrary, we have been informed that these Crypto Capital amounts are not lost but have been, in fact, seized and safeguarded. We are and have been actively working to exercise our rights and remedies and get those funds released.”

Yet Crypto Capital isn’t showing any signs of life. Fortune requests for comment sent to the contact email on its website went unreturned. Common sense says that if the website were still being maintained, someone might have scrubbed Quadriga’s name from it after that exchange declared bankruptcy in February. Perhaps law enforcement authorities have shut down the firm and seized the funds, but in that case, it’s not clear which government is holding them, and the legal avenues to recovering them are likely long and complicated—particularly when Bitfinex itself is incorporated in the British Virgin Islands.

I would, however, wager that the Crypto Capital mystery extends farther than just Bitfinex and Quadriga, and I wouldn’t be surprised if it shows up in more prosecutors’ lawsuits.

***

We’ve released a preliminary agenda for Fortune’s inaugural Brainstorm Finance conference in Montauk June 19-20—you can check out the program here. Conference attendance is by invitation only, but you can request an invite by emailing me directly.

GOT TIPS?

Send feedback and tips to ledger@fortune.com, find us on Twitter @FortuneLedger or email/DM me directly at the contact info below. Please tell your friends to subscribe.

| Jen Wieczner | |

| @jenwieczner | |

| jen.wieczner@fortune.com |

THE LEDGER'S LATEST

NYSE Owner Buys Crypto Custodian in Latest Push to Offer Bitcoin by Jeff John Roberts

What Happened to the Winklevii After Facebook by Rachel King

Bitcoin Tumbles After Officials Allege $850 Million Fraud by Jeff John Roberts

5 Numbers to Watch to Spot the Next Recession by Jen Wieczner, Rey Mashayekhi, Lucinda Shen, Erik Sherman, Shawn Tully, and Nicolas Rapp

Coinbase Shuts Chicago Office as Crypto Slump Continues by Jeff John Roberts

DECENTRALIZED NEWS

To the Moon… Societe Generale issues $112 million in bonds on the blockchain. Stripe makes an acquisition. Pinterest's first employee is now putting art on the blockchain. The first clearinghouse for cryptocurrency derivatives is launching in Singapore. TD Ameritrade is apparently testing Bitcoin and Litecoin trading...and E*Trade is close to launching it too. Venmo now has more digital users than Bank of America or Wells Fargo.

…Rekt. SoftBank founder Masayoshi Son bet big on Bitcoin at exactly the wrong time. JCPenney cuts the cord on Apple Pay. Antivirus entrepreneur John McAfee promised to reveal the identity of Satoshi Nakamoto...then quickly went back on his word. Mike Novogratz's firm Galaxy Digital lost almost $273 million on its crypto investments last year. Bitcoin is "still a few years from any sort of clarity about where this technology will fit in the world." Crypto publication BreakerMag shuts down.

BALANCING THE LEDGER

On the latest episode of "Balancing the Ledger," Jonathan Levin, co-founder and COO of Chainalysis, discusses criminals' favorite cryptocurrency at the moment, how blockchain analysis has led to more arrests of opioid dealers, some disturbing findings about the Quadriga exchange situation, and more.

BUBBLE-O-METER

Attacking the honeypot. While cryptocurrency certainly has its share of scams, it turns out cybercriminals are increasingly attacking financial firms across the board. A new report by cybersecurity firm Proofpoint found that email attacks on financial services companies in which fraudsters pose as legitimate senders (known as imposter attacks) increased 60% in the fourth quarter of 2018 compared to a year earlier.

It's something we've experienced firsthand at The Ledger—and we don't even sit on the mounds of capital that banks do. As always, be careful out there, particularly when clicking on emails.

MEMES AND MUMBLES

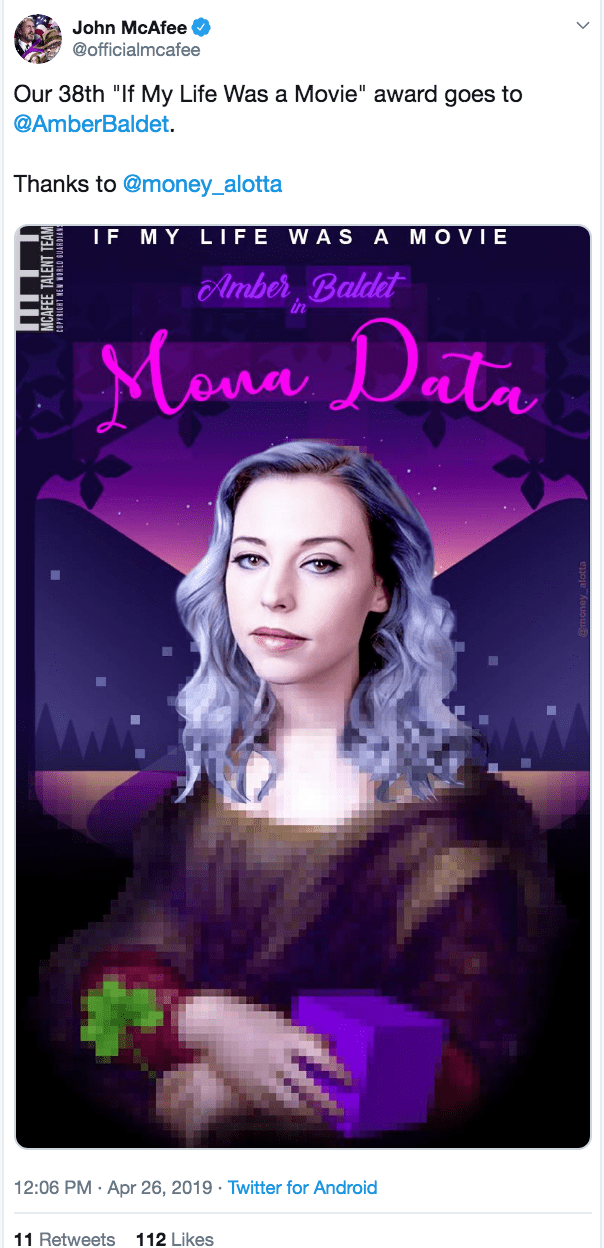

If your life was a movie. For more than a month, John McAfee—the same John McAfee behind McAfee antivirus software who also recently claimed to know who Satoshi really is—has been bestowing a peculiar honor upon unsuspecting characters in the crypto space and beyond. So far, McAfee has handed out more than three dozen "If My Life Was a Movie" awards to recipients from Ethereum creator Vitalik Buterin to Tesla CEO Elon Musk, tweeting out fake movie posters based on each honoree's life.

McAfee on Friday awarded his 38th and latest prize to Amber Baldet, the co-founder and CEO of Clovyr. The poster more closely resembles a Renaissance painting (da Vinci's "The Mona Lisa") than a film promo, but oh well—this particular so-called awards contest doesn't really seem to have any rules.

As Baldet tweeted in response, "Every so often the universe lays a small gift at your feet and whispers softly: bet you didn’t see this sh*t coming."

We hope you enjoyed this edition of The Ledger. Find past editions here, and sign up for other Fortune newsletters here. Question, suggestion, or feedback? Drop us a line.