In this era of unprecedented, global monetary stimulus, markets hang on every word central bankers utter.

Central bankers, however, are less interested in financial markets. If you ask Janet Yellen, for instance, she’d say that the stock market is one “transmission mechanism” through which monetary policy affects the real economy. Yes, low interest rates will indirectly lead to higher stock valuations, but the central bank’s real aim is to simulate the real economy by encouraging businesses to invest and consumers to spend.

James Montier of the investment management firm GMO, however, argues that central bank policy never makes it to the real economy. In a paper published this week, Montier argues that the economics and investment communities “idolatry” of interest rates is the “greatest con ever perpetrated.” Writes Montier:

There seems to be a perception that central bankers are gods (or at the very least minor deities in some twisted economic pantheon). Coupled with this deification of central bankers is a faith that interest rates are a panacea. Whatever the problem, interest rates can solve it. Inflation too high, simply raise interest rates. Economy too weak, then lower interest rates . . . This obsession with interest rates as a cure-all rests on some dubious views about the way the world works. First, is an interest rate cut expansionary or contractionary with respect to spending? Those who believe interest rates are an effective tool clearly believe a rate cut is expansionary because it reduces the cost of financing and then stimulates demand (via investment, consumption, and/or net exports). This emphasises the obvious but oft unspoken truth that monetary policy works via the debt channel (or reducing savings, which is the same thing as increasing leverage).

Montier argues that, actually, interest rates have very little bearing on corporate and individual investment and consumption decisions. Take a look at the following charts. The first shows that corporate investment is generally financed with internal funds, rather than debt:

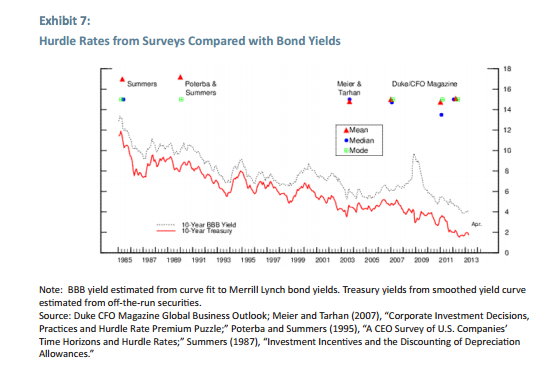

Here’s another showing interest rates over time, combined with surveys showing “internal hurdle rates” for investment projects. Regardless of where interest rates are, companies generally require a 15% rate of return when embarking on a new investment:

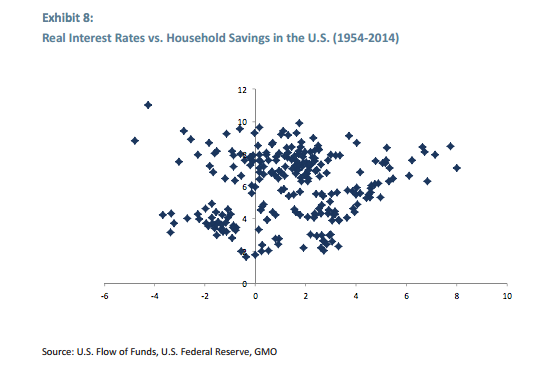

Finally, Montier argues that there isn’t a strong correlation between household savings rates and interest rates:

“It would appear that monetary policy isn’t the most effective tool for managing the economy,” Montier writes. “I am well aware that almost everyone reading this is likely to disagree: that is the nature of the greatest con ever perpetuated.”

Montier argues that fiscal policy is the only way for the government to meaningfully manage the economy, but it is ignored for “political rather than economic” reasons. He postulates that business groups are wary of the idea that direct government spending could support employment or play too large a role in the economy, because that require the business community to relinquish power.

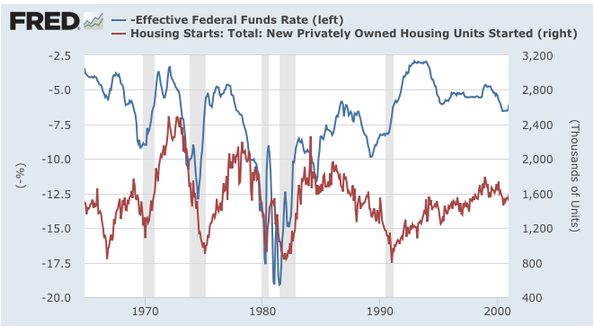

Economist and New York Times columnist Paul Krugman took umbrage with Montier’s analysis, despite the fact that these two seem to agree on Montier’s larger point that government spending should play a bigger role in propping up the economy. But Montier lumped Krugman in along with economists like Ben Bernanke and Janet Yellen who place too much faith in the power of monetary policy to manage the economy. Krugman struck back in a blog post, arguing that while interest rates may not affect business investment, they do have a major effect on housing:

Krugman points to the strong correlation between housing construction and interest rates. Housing is a long-term investment in which the cost of money adds up to quite a lot over time. That’s a lot different than, say, a company’s decision to invest in smartphones for its employees.

So, perhaps Montier overstates his case. But it is striking to see the many ways in which monetary policy doesn’t touch the real economy. It’s been common among the economic commentariat to lament that the Fed is the only institution in Washington that has the freedom to experiment with stimulus, because of gridlock in Congress. But the Fed’s own impotence may allow it such freedom. Sure, Fed policy creates a lot of controversy. Members of Congress are known to wax apocalyptic about the effects of quantitative easing. But even the Fed itself admits that its trillions of dollars worth of bond buying has had, at best, a slightly positive effect on economic growth.

Fiscal policy on the other hand, is potent. And the American government–with its numerous checks and balances and veto points–is pretty good at preventing the wielding of power. Whether you believe more in the power of tax cuts or in infrastructure spending, changes in fiscal policy will have a powerful effect on the economy and create winners and losers. Monetary policy, on the other hand, is perhaps more like a placebo, that may help boost confidence but doesn’t come with too many unsavory side effects.