Editor’s note: This article was originally published in the September 19, 1994 issue of Fortune.

To get a taste for the crazy ways marketers must compete for today’s finicky consumer, stroll through the beer section of your local retailer. You’ll see Icehouse, a successful new upscale beer from Plank Road Brewery –a fake parentage concocted by Miller Brewing to give a microbrewed image to suds produced in megabreweries. (Call it phantom branding.) You’ll also find Killian’s Irish Red, a pseudo-import made by Coors Brewing in Golden, Colorado, and Zima, a weird, colorless malt beverage that Coors positions as “something different.” You can buy any of these oddball drinks for about $5 per six-pack. On the other hand, if you’re in California this Labor Day weekend, you can use a mail-in coupon to binge on 12-packs of Budweiser, the so-called King of Beers, plus Coors and Miller, its broad-shouldered rivals, | for just $1.99. That’s right, less than 17 cents a can.

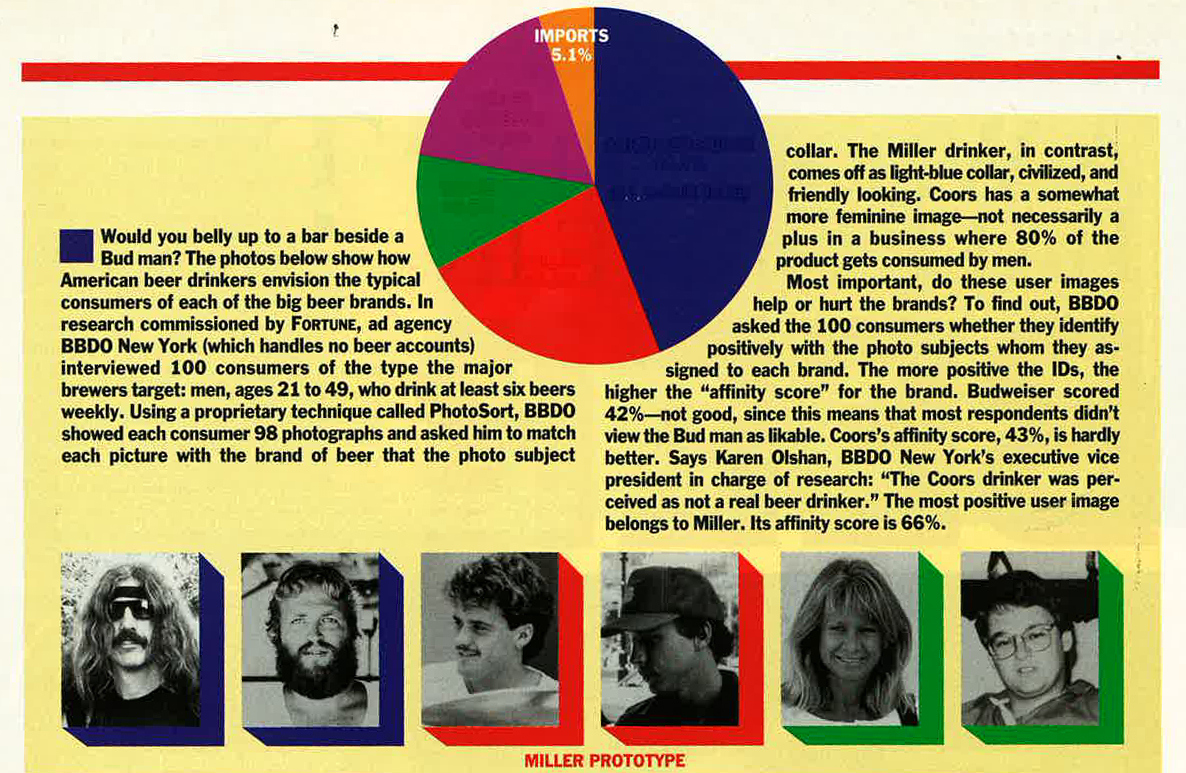

Are these trends in any way related? Yes. Heavy discounting of famous-name beers and the proliferation of peculiar, high-priced new ones both flow from the same source: Big brands are losing their fizz. Original Coors’s volume is less than one-third the level of the mid-1980s. Budweiser, which accounts for more than half Anheuser-Busch’s $8.7-billion-a-year in beer sales, saw its volume sink 9% from 1990 through last year, while Miller’s heavyweight brand, Lite, was off 16%. With big-brand images in trouble (see box), beer bosses are cutting prices to lure consumers even as they scramble desperately to develop or buy the types of beer that American drinkers will pay more for — imports, whose sales rose 11% last year, and microbrews, whose tiny 1% market share is nonetheless expanding at an eye-popping 50% annual clip.

The result of all this ferment, says Michael Bellas, president of Beverage Marketing in New York City, is that “the U.S. beer industry is going through a sea change I haven’t seen in 20 years.” And when change of that magnitude roils a market, heads usually roll as well. At No. 2 Miller, owned by Philip Morris, and at Coors, at least 70% of the top 15 or so management positions have changed occupants in the past year alone. More than half the newcomers are from outside the beer business.

For new and old alike, the central question posed by beer’s new brand game is this: How does a multibillion-dollar company create products to compete against little guys — and simultaneously protect its big established brands? The answers are relevant to marketers in any industry.

Obvious Step One: Innovate. True, no one sees anything revolutionary on the horizon. Says Anheuser-Busch CEO August Busch III, 57: “I don’t think there’s going to be a completely new way to make beer or a breakthrough as there was in the Seventies with light beer.” But this year the industry has introduced about 40 — count ’em — new “ice” beers. Pure gimmickry? You bet. Ice beers, first developed in Canada, are beers produced at temperatures just a few degrees colder than ordinary brew, which gives them a slightly above-average alcohol content. Still, “ice” has turned out to be one cool marketing ploy. The products have captured almost 6% of industry sales — more than all imports combined.

Among the major players, the most dynamic — and desperate — transformation is taking place in the malt-scented valley of Golden, Colorado. Here Coors last year imported the first nonfamily member in its 121-year history to run its beer business. As head of a vulnerable No. 3 in a flat market where more than 700 companies have gone out of business in the past 50 years, CEO Peter Coors, 47, admits that he’s pursuing a survival strategy. Of his decision to seek outside help, he explains simply, “I wasn’t smart enough to know what to do. I needed professional management.”

YOU’D SURE never mistake new president W. Leo Kiely III for a Coors family member. Unlike that skinny, conservative, low-key crowd, Kiely, 47, is a rambunctious independent with a beer-barrel body. Despite appearances, though, he’s no lifetime brew man. Kiely spent the previous 11 years at PepsiCo’s Frito-Lay unit, where he rose to president of the central U.S. division and was a candidate to head the entire Frito-Lay company. Hired with a mandate to shake Coors up, Kiely has replaced seven of the top nine managers (one position, chief financial officer, is yet to be filled). His goal: to pump up Coors’s unpredictable but consistently lousy return on investment (4% last year) to at least 10% in three years.

To do that, says Kiely, “we need to be innovative in everything we do.” Coors, already an impressive technical innovator (it introduced the first aluminum can and the first cold-filtered beer, both in 1959), especially needs to become a more creative marketer. Kiely has scored a minor hit by launching the Colorado Silver Bullets, the first all-female professional baseball team since the 1950s, to promote Coors Light. The team’s record is terrible (5-37 against all-male, minor-league, and semipro opponents). But unexpectedly large crowds are turning out to root for the underdogs.

Hitting a home run looks much less likely. A possible model: George Killian’s Irish Red, a thoroughly American beer that gets no TV advertising but by dint of its clever name (Coors licensed it from a long-defunct brewer in Enniscorthy, Ireland, in the early 1980s) is stocked in retailers’ import cases and commands a high price. Killian’s is now neck and neck with Samuel Adams as the largest specialty beer in the U.S. Coors’s bigger bet is Zima, a clear drink whose zigzag performance shows just how risky product development can be. “Zima is a sexy new product,” insists Kiely, who accelerated its rollout this year. Cleverly advertised as a mystery drink with “zecret ingredienz,” fizzy, foam-free Zima is tremendously successful in new markets, where 70% of alcoholic-beverage consumers — including women who don’t drink beer — typically try it. But sales quickly sink because, sigh, people don’t like the stuff very much. Some choice samples from an informal FORTUNE survey conducted over the Internet: “Zima zucks,” and it tastes like “tonic water, antifreeze, and crushed SweetTart candies mixed with skunked (translation: spoiled) Molson.”

Zima may give Coors a brief but pleasurable buzz. Wall Street is projecting a 50% rise in profits this year, thanks mainly to its national debut and the 50%-plus growth of Killian’s. But even Pete Coors holds little hope that Zima is anything more than a fad. “Anheuser-Busch and Miller have sophisticated market research, and if they thought that (clear malt drinks) were going to be a major category, they’d be in it today,” he says. They’re not. And they don’t plan to be.

When it comes to finding new ways to grow by developing, testing, and delivering new products more quickly and efficiently, the people at Miller have the smartest ideas these days. Says CEO Jack MacDonough: “I have two rallying cries: fast cycle time and very local marketing attention.”

Miller certainly needed a kick when MacDonough, 50, a former top marketer at Anheuser-Busch, came aboard two years ago. The company’s market share has been stuck in the low 20s since 1980. MacDonough swiftly broadened Miller’s portfolio of brands by buying Molson Breweries U.S.A. (the import arm of the Canadian brewer) and raised its output of new brews from an average of two per year toseven this year.

Jack is nimble. Jack is quick. By getting Miller’s new Icehouse and Lite Ice widely distributed before Anheuser-Busch launched comparable brands, MacDonough has captured over 50% of ice beer sales in supermarkets. Anheuser’s share is 29%. Coors, late to the market with its Arctic Ice, is available in only 30% of the U.S.

That quickness reflects fundamental changes MacDonough made in the way Miller markets. Case in point: a shift to momentum marketing, so-called because the process gets new beers flowing to consumers quickly. This enabled Miller to test its Icehouse beer inexpensively — $500,000 vs. $12 million for a comparable new product tryout last year.

WITH MOMENTUM marketing, instead of mounting one or two full-scale product trials each year — which require costly TV commercials and retail displays — you conduct half a dozen simple tests. Through its wholesalers, Miller ships prototype brew and promotional materials to 15 or so bars and restaurants in a few select cities. Miller marketers unobtrusively hang out at the test sites, observe, interview bartenders, and then do phone surveys of customers who fill out cards at the bar. Most products fail initially. In July, Citro, a lime-flavored beer, flunked its first eight-week momentum marketing tests in San Diego and Gainesville, Florida. So Citro has gone back to Miller’s laboratories to get revamped. MacDonough’s second change was to decentralize his sales organization. Says Richard Strup, 41, Miller’s marketing chief: “Practically every decision used to be approved by the senior vice president of marketing in Milwaukee. I knew when I got a request to okay 15 neon signs in El Paso that this was no way to run a business.” That feeling was reinforced when Miller last year benchmarked companies that sell through distributors — Coca-Cola, Pepsi, Gallo, the automakers — and found that the most successful allow local managers to run their own shows.

In January, Miller divvied up the U.S. into 19 regions and will give this shift added oomph by linking each general manager’s pay to his region’s performance. Says President John Bowlin, 43: “In the spirit of empowerment, when we launched Icehouse, we didn’t set a price. We asked each market, ‘How much can you get for this product? You price it.’ ” The sales teams in the southeastern U.S. opted for an atypically high, almost import-level price, and the Southeast is now Icehouse’s hottest market.

The third big change at Miller is moving to a more flexible manufacturing system. “For years we had essentially two brews, Miller High Life and Miller Lite, and production was nice and straightforward,” says Bowlin, who was president of Philip Morris’s Oscar Mayer company until last year. “Now we have to think, ‘How can we produce to order?’ ” To get ideas, Bowlin and some operations managers traveled to the small town of Capehill, England, on the outskirts of Birmingham. There they studied how Bass Brewers, Britain’s leading beermaker, had refashioned its brewery to handle multiple, low-volume products. They concluded that Miller didn’t need a new brewery with small kettles and flexible production lines. Instead, the company is spending more than $500 million through 1998 to retool the six big plants it’s got (a seventh, in Fulton, New York, is shutting down on September 30). One early sign of progress: Shifting production from one beer to another, which used to take four hours, now takes one.

Left unanswered by this frenzy of innovation and proliferation, however, is the critical question of how you expand a venerable but tired brand. Miller’s 21-year-old Lite (38% of company volume) has lately been losing drinkers to 12-year-old Bud Light, which has better advertising and is winning new light- beer drinkers. For now Miller is propping up the franchise with Lite Ice and shifting national marketing money to the local level to compete more nimbly against regional brands. That means, for instance, that Lite now gets plenty of television ad support in Houston, where it is the market leader. But in Portland, Oregon, where regional and European-style microbeers are the craze, local bosses have chosen to spend zero on TV ads touting their company’s mainstay.

One thing is certain: While throwing money at a market may not capture much extra share for older brands, in a business that’s built on froth, cutting your marketing investment sharply is a sure-fire formula for disaster. Just ask Coors, which until recently had been supporting Coors Light, its best seller, and Zima at the expense of Original Coors. Indeed, last year’s $4 million in ad support was a mere one-tenth of what it spent on its flagging flagship brand in 1985. Drawing the obvious conclusion, senior vice president of marketing William Weintraub, 51, a newcomer from Tropicana, is tripling Original Coors’s ad budget this year. Says he: “This industry seems consumed by the vortex of doom phenomenon — the belief that every old brand is going to die. But I genuinely think ours can be turned around.”

That vortex of doom is Worry No. 1 at Anheuser-Busch, which has the most big, aging brands to protect. Behaving typically market leaderlike, Anheuser, with a commanding 44% of U.S. beer sales, has laid relatively low in the new- products game. Says August Busch IV, 30, vice president of brand management, son of August III, and heir apparent (the family still controls 8% of the stock): “The breweries that we have are designed to produce big brands. Our system is set up to sell big brands. Our competition can’t compete with big brands. That’s why they’ve had to introduce lots of little brands.”

Tough talk for an unproven marketer whose ascension happened sooner than planned last March, after his predecessor unexpectedly departed. And even Busch admits that the kind of ferocious price war now under way in California, while it may intimidate smaller rivals, is hardly the message he’d like to send consumers about his company’s franchise Budweiser brand. Says he: “It’s the worst thing in the world for brand image.”

Critics contend that young August, though eager and reasonably smart, isn’t up to the job of turning Budweiser around. But August III, whom his son calls “Chief,” is confident his boy can help Bud develop a much needed younger image. So far, though, he hasn’t done much to draw twentysomethings to the brand. What he is doing is spending $2 million to sponsor the current U.S. concert tour of the wizened but durable Rolling Stones — “the kings of rock & roll with the king of beers,” he says — and scrapping a disappointing 18- month-old TV campaign with the theme “Proud to be your Bud.”

Of the new one, due out in October, August IV spills few details. “It’ll focus more on quality,” he says. “It’s a variation of ‘this Bud’s for you’ for the Nineties. It’s awesome. A really cool idea.” As Busch strives to meet his goal of arresting Bud’s market share slide by next year, his company has hedged its bets by buying a minority stake in Redhook Ale Brewery, a Seattle microbrewery that sold 76,000 barrels of beer last year, vs. Anheuser’s 90 million. Still, the deal has drawn cheers from Anheuser’s distributors, who are desperate to push higher-margin, prestige brands.

FOR REDHOOK, the largest microbrewer without national distribution, Anheuser’s investment is a ticket to coast-to-coast selling. CEO Paul Shipman, 41, says that during negotiations early this year, August Busch III “grabbed a pad of paper, and with one quick sweep he drew a map of the U.S. Then he said to me, ‘Put X’s where you want to build breweries.’ ” Shipman, intoxicated by opportunity, drew five.

Since Anheuser disclosed its Redhook deal, other giants — among them Miller and Seagram, which is not even in the beer business — have reportedly been sniffing out investments in microbrewers. That prospect troubles specialty beermaker Jim Koch, 45, whose Boston Beer Co. makes Samuel Adams and who has no interest in hawking his brew with Fortune 500 help. “I’m afraid of the big guys,” he says. “They have the power to dominate any segment they want. Still, my faith is that better beer will win out.”

Relax, Jim. The good news is that’s exactly what seems to be happening as consumers migrate away from the bland megabrands to tastier prestige labels. So if the beer barons really do draw the right lesson — and either ape your – success or buy out guys like you — well, shouldn’t beer lovers all raise a glass to that?