These stocks and funds should do well even if interest rates keep rising.

Remember June 2006? Uber didn’t exist; neither did the iPhone. Lehman Brothers was humming along, and rising housing prices were beginning to take what America thought would be a “breather.” That month the Federal Reserve, chaired by a newbie named Ben Bernanke, bumped up the Federal funds rate 25 basis points, to 5.25%. It would be the last rate hike for more than nine years.

Since then a financial crisis has come and gone, and a jobless rate that reached 10% has fallen to 5%. But the funds rate—the Fed’s principal lever for controlling interest rates systemwide—now sits close to zero, where it came to rest in 2008 as the Fed pumped up the economy. Investors, fearing the impact of a rate hike on stocks and bonds, are sweating bullets about when rates will tighten. Most believe the Fed will raise rates incrementally in mid-December (by the time you read this, it may have done so), but Fed insiders have offered zero clarity about what will follow, fretting publicly about whether signs of a strengthening economy outweigh looming threats. The Fed “might [raise rates] 25 basis points and go away well into spring,” says Greg Valliere, chief strategist at Horizon Investments, a firm that manages $2.4 billion. “It’s the most dovish Fed in our lifetime.”

“The persistence of the low-rate environment is not what people expected at the start of the year,” adds Russ Koesterich, BlackRock’s chief investment strategist. And that persistence is a problem for many money managers—indeed, a whole generation of investment pros was in college the last time rates went up.

[fortune-brightcove videoid=4646527272001 height=”484″]

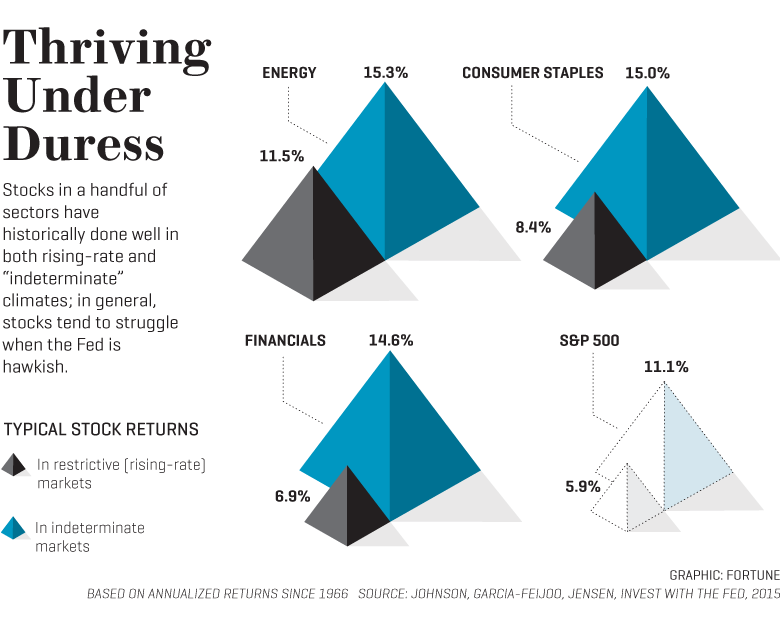

Still, savvy investors can find guidance in history. Or so says Bob Johnson, president and CEO of the American College of Financial Services. With Gerald Jensen of Creighton University and Luis Garcia-Feijoo of Florida Atlantic University, Johnson recently surveyed the years 1966 through 2013 to determine which stocks perform best during which monetary-policy cycles; they published their findings this year as the book Invest With the Fed.

They concluded that trends in rates—up or down—are more important to asset prices than how much rates move. Right now, rates seemingly can only go up, which would typically make this what economists call a restrictive period, when equities perform badly. But because the Fed has vacillated—it has “virtually no conviction around its move,” Johnson says—today’s environment is more akin to what he calls an indeterminate period, when Fed signals are mixed and rates don’t trend one way or another. Indeterminate periods, it turns out, aren’t rare. Roughly 17 of the 48 years covered by Johnson’s study qualify. Better yet: Johnson and his colleagues have identified stock sectors and asset classes that have performed well in such murky conditions.

Fortune took their research as a jumping-off point, looking at sectors that thrived in indeterminate years. Because history seldom repeats itself exactly—even Johnson acknowledges, for example, that today’s low rates are “unprecedented”—we asked investors which stocks in those sectors could do well in today’s particular economic circumstances. And we narrowed our search to sectors that also outperformed in rising-rate climates, in case the Fed turns unexpectedly hawkish. The result: investment picks that could hold up regardless of where rates go in 2016.

Energy

Under normal circumstances, buying energy stocks today would be an easy call. According to Johnson’s research, energy is the best-performing sector during indeterminate rate cycles, averaging a 15.3% annual return; energy stocks also thrive when rates are rising, gaining 11.5% (see chart). Both those rate climates correlate with a growing economy, which usually means more energy consumption. What’s more, energy companies generally do well in inflationary environments, says Dirk Hofschire, senior vice president of asset allocation research at Fidelity.

The problem, of course, is that the energy sector is anything but normal today. A slowdown in China and overproduction elsewhere have created a huge oil glut, sending crude prices and the stocks of energy companies plummeting. Dan Katzenberg, oil-stocks analyst at Baird Equity Research, estimates that the industry is producing 2 million more barrels of oil per day than the world is consuming. Still, he sees some encouraging signs: He estimates daily demand will grow by 1.2 million barrels over the next year; at the same time, U.S. producers have sharply cut production from its April 2014 peak. “That gets us pretty close” to equilibrium of supply and demand, he says.

Until then, companies that can keep their costs down will fare best in a cheap-energy world. Katzenberg likes companies with “core shale acreage” from which they can extract oil and gas cheaply. He favors Whiting Petroleum (WLL), whose operations in the Bakken and Niobrara fields in the Great Plains fit that description. He thinks Whiting could be worth 44% more than its current price as it divests noncore assets. Katzenberg also likes EOG Resources (EOG), which has a strong cash position and low-cost reserves in Texas and the Rockies as well as the Bakken, and Pioneer Natural Resources, whose assets in Texas’s Midland Basin he sees as particularly valuable.

Chip Rewey, lead portfolio manager at Third Avenue’s flagship Value Strategy Fund, thinks that energy producers with strong cash positions will have an advantage if oil and gas prices stay low, because they won’t face pressure to ramp up production or sell off assets. Rewey singles out Devon Energy and Apache Corp., (APA) both of which have net-debt-to-Ebitda ratios much lower than those of oil “super majors” like Chevron and Exxon Mobil. Both companies have the capability to be “profitable at $40 oil,” Rewey says.

Financials

Because banks and financial services companies earn more on deposits, loans, and other assets when interest rates are higher, investors assume they’re great investments when money tightens up. But financials actually do better during indeterminate cycles, returning 14.6% annually, compared with 6.9% in rising-rate climates. One reason for that disparity: Investors often crowd into the stocks in anticipation of rising rates, so stock gains come before the rate hikes do. (Recent trading bore out that pattern: Between mid-October and mid-November, a basket of bank stocks tracked by Bloomberg rose 6%.)

[fortune-brightcove videoid=4600298867001 height=”484″]

The best way to capture the financial-stock advantage in the current climate is to find companies that benefit disproportionately from even a small bump in rates. Rewey of Third Avenue likes BNY Mellon. With rates low, Rewey notes, BNY has had to grant fee waivers on money-market accounts to keep investors’ returns positive. When rates climb, it can discontinue those waivers, adding 12¢ to 15¢ to its annual earnings per share for every 0.25% increase in the Federal funds benchmark. Overall, Rewey says, higher rates would boost BNY’s earnings by almost a third. Another factor in BNY’s favor: It has very healthy cash reserves, which will enable it to continue to support stock buybacks and dividends. Even “if the growth isn’t there … economically they are returning capital,” Rewey says. Once rates do rise, he thinks the stock could be worth more than $60, a 37% premium to the current price.

Investment giant Charles Schwab has also been granting fee waivers to savers and should benefit when that practice ends. Mitch Rubin, co–chief investment officer of RiverPark Funds, which manages $3.8 billion, says a 150-basis-point increase in rates over the long term would increase Schwab’s earnings by 50%. (For more on the case for Schwab, see “Good Stocks for Bad Times”.)

Consumer Staples

Companies that make and sell basics like diapers, shampoo, and groceries can often sustain their sales regardless of the economy’s ups and downs. And Johnson’s research shows that this sector was the second-best performer in both indeterminate- and restrictive-rate climates, trailing only energy.

These days, however, consumer-staples investors need to be discerning. Chris Sunderland, equity institutional portfolio manager at Eaton Vance, notes that because rates have been low for so long, investors have flocked to these stocks for their dividends, driving up their prices. And if inflation rises, he says, these companies will face higher expenses and “their price-to-earnings multiples will contract.”

Companies in the sweet spot today have both the growth potential to justify their current stock prices and the power to pass on cost increases to customers. And stores that sell consumer staples look better on these fronts than the companies that make them. Rubin of RiverPark says dollar-store chains are particularly good at passing along costs—for example, by cutting the overall size of a product rather than changing its price. Rubin favors Dollar Tree (DLTR), whose core business has operating margins “in the mid-teens” in the U.S. and is growing faster than competitors. Margins aren’t as high at Family Dollar, the rival chain that Dollar Tree acquired in January 2015, but Rubin thinks that profits will grow as the chains’ integration progresses.

Joseph Agnese, analyst at S&P Capital IQ, likes Kroger. The supermarket giant has bulked up through acquisitions, most recently making a deal to buy Midwestern grocery conglomerate Roundy’s, and its scale has helped it boost market share and keep up in price wars with Walmart and other big-box competitors. At the same time, Agnese says, Kroger has “gained consumer loyalty with service offerings like a fishmonger and a bakery” and expanded its organic offerings—touches that give it leeway to charge higher prices. Agnese says the stock could be worth $47 a share, or 25% higher than its current price.

Value stocks and funds

Historically when interest rates have fallen, “the tide has lifted all boats,” says Sunderland. “No longer will this be the case when we see rates going up.” In those circumstances stocks with lower prices relative to their earnings—value stocks, as pros label them—tend to outperform. Patrick O’Shaughnessy, principal and portfolio manager at O’Shaughnessy Asset Management, says that the 10% of stocks that are the cheapest by his measures have outperformed the broader market in all but three of the past 17 periods in which the yield on the 10-year Treasury rose by more than 1%. Johnson’s research backs this up: During indeterminate periods, large-cap value and small-cap value stocks steadily beat their growth-stock counterparts. When rates rise, that advantage goes away among large-cap stocks but remains in effect for small-cap and midcap stocks.

The easiest way to play a tilt toward value is to invest in mutual funds. Among actively managed funds, Todd Rosenbluth, director of ETF and mutual fund research at S&P Capital IQ, recommends Dodge & Cox Stock for large-cap stocks and Vanguard Explorer Value for small-caps. Each has relatively low expense ratios, and each has bested peers by about two percentage points annually over the past five years.

Exchange-traded funds offer a cheaper way to pursue the trend, with investments that track benchmark value indexes. The Vanguard Value ETF has an expense ratio of 0.09% and has risen 6.5% annually since its inception in 2004; the iShares Russell 2000 Value ETF, which focuses on small-cap stocks, has expenses of 0.25% and has returned 8.6% annually since 2000.

And surprise! Even some bonds

Rising rates give bond investors migraines, and for good reason: As rates rise, the value of existing bonds drops, since the interest they pay no longer looks as competitive. But if rates rise only gradually, the decline in bond prices might not be as painful, says Fidelity’s Hofschire, and if rates rise slowly and stocks struggle, “bonds could be a safe haven.”

Gemma Wright-Casparius, senior portfolio manager with Vanguard’s fixed-income group, says investors should favor shorter-duration bonds when rates rise—because they can reinvest their money in higher-yielding instruments as their older bonds expire. Short-term-bond prices are also less volatile than those of longer-term bonds in rising-rate climates. Johnson’s research team found that three-month Treasury bills returned 6% annually during such periods, with only about two percentage points of price volatility. (Longer-term Treasuries and investment-grade corporate bonds had comparable returns, but much greater price fluctuation; that may not be a cause for concern for those who don’t need to tap their portfolio anytime soon.)

Among funds focusing on short-term bonds, Rosenbluth of S&P Capital IQ likes DoubleLine Low Duration, which outperformed funds in its category by 0.6 percentage points a year over the past three years, and the Vanguard Short Term Bond ETF, which has an expense ratio of just 0.10%.

A version of this article appears in the December 15, 2015 issue of Fortune with the headline “How To Fight Your Fear of the Fed.”

For more features from Fortune’s Investor’s Guide, click here; for more online Investor’s Guide coverage, click here.