A joke was making the rounds a few years ago in China: If a U.S. startup had a great idea, Google might buy it. If a Chinese startup had a great idea, Tencent might copy it.

That last thought crept into Wu Hao’s mind late last year when Tencent, China’s social media and online games giant, came calling. Wu’s food delivery startup, Line0, was raising money, and Tencent wanted a stake. “At first we were concerned they had ulterior motives,” says Wu, an energetic 32-year-old who started his business in China’s old capital, Nanjing. Wu was worried that his yellow-uniformed deliverymen, who jet across China’s cities on electric scooters, would be absorbed and copied by a web giant with $13 billion in revenue.

But Tencent’s venture capital team pitched Wu hard. They met with him five times, grabbing dinner with him at restaurants on the Line0 system. They told Wu that Tencent understood the ecosystem of “online to offline” companies like Line0—companies whose apps enable consumers to buy real-world goods and services. They had already invested in similar companies like Dianping, the Chinese equivalent of Yelp. They also reassured him about the future, when Tencent might propel Line0 in front of a half-billion potential new customers—the users of Tencent’s gargantuan social network, WeChat.

What Tencent didn’t need to tell Wu was that it was investing in startups faster than almost anyone else in the world. If Wu said yes, Line0 would join four dozen companies Tencent backed in 2014. Tencent didn’t generally buy companies outright, but it had shown it would bolster them with very big checks.

Wu didn’t want to miss his shot. In January, Line0 received $30 million in a financing round led by Tencent. In return Tencent got the chance to add Line0’s nearly 1 million users to its online payment network—the central element of the company’s battle plan in China’s fast-evolving Internet wars.

2014 Company Profile

Revenues: $12.8 billion

Profits: $3.9 billion

Employees: 27,690

Total return to shareholders (2005-15, annual rate): 61.8%

China’s biggest tech companies are in the middle of an uncertain transition. The country’s three Internet giants—Baidu (BIDU) in search, Alibaba (BABA) in e-commerce, and Tencent (TCEHY) in social networking, known collectively as BAT—each became a profitable, multibillion-dollar empire on the strength of its core business. (Baidu had $8 billion in revenue in 2014, and Alibaba $12.3 billion—making both, like Tencent, big enough for the Fortune 500, though not the Global 500.) But as their growth has slowed, the Big Three have shifted into a new mode, spending billions on venture funding and acquisitions that could help them further expand their reach and their revenue. “Before it was, ‘We can build it better ourselves,’ ” says Richard Robinson, a China-based entrepreneur and investor in startups, describing the BAT’s attitudes. “But now that means you’re behind.”

In this land rush no company has been more aggressive than Tencent. Last year the company invested in four of China’s 10 largest tech venture deals and took part in a total of 48 deals worth $6.3 billion, according to Preqin, an alternative-assets data company; by that measure, Tencent was a bigger venture capital player than Alibaba or Baidu or, for that matter, Google. The deluge continued this year: Through April, Tencent had joined another $4 billion worth of deals.

Just as striking, however, is Tencent’s eagerness to make small deals like the Line0 play, investing seven-figure sums in modest ventures like travel agencies and cleaning services. It’s a bit like China’s effort to expand its territory by building islands atop tiny reefs in the South China Sea: It can look quixotic, until you consider the big picture and the long-term stakes.

Known for avoiding the press, Tencent declined Fortune’s repeated requests for interviews with executives. But in conversations with more than a dozen companies Tencent has backed, and with former Tencent employees, consultants, and analysts who follow the company, a clear strategy emerges: a quest to make Tenpay, and by extension Tencent, dominant in online finance.

Tencent wants to create a socializing and shopping universe that users never have to leave. That means investing in dozens of retailers and service providers and connecting them with hundreds of millions of potential customers on WeChat. More important, it means controlling the payment system that links this universe together—which could add billions of dollars to Tencent’s top line. Tencent generally doesn’t take controlling stakes in the companies it funds, but it expects startups to use Tenpay, analysts say. Lately the pay network and the web of Tencent-backed ventures have grown in tandem: The company now says more than 100 million WeChat accounts are linked to bank accounts—some observers think the actual number is double that—up from almost none at the beginning of 2014.

Online payment systems and their partner marketplaces have piggybacked before. (Case in point: eBay (EBAY) and PayPal, which investors valued at more than $40 billion when it spun off in July.) And Tencent is very much playing catch-up with rival Alibaba, whose Alipay service dominates China’s mobile-payment market.

But given that online finance looks like the next great opportunity in China’s 650 million–user Internet market, and that growth in Tencent’s core PC game division is slowing, the business is too good to miss. “If you own payment, it’s like owning the app store on iOS or Google,” says HSBC’s (HSBC) China Internet analyst, Chi Tsang. “You collect a percentage on everything.” Take the analogy a little further, and it could be like owning a new MasterCard (MA) or Visa (V)—in a huge market where consumers are just growing accustomed to using credit cards.

Unlike Alibaba (widely viewed as the Amazon (AMZN) and eBay of China) or Baidu (China’s Google), Tencent doesn’t have a clear American web equivalent. The company is a social platform like Facebook (FB), an online games giant with bigger sales than Zynga in its heyday, and a video and news site similar to the Huffington Post—lately with a VC firm like Andreessen Horowitz grafted on.

It’s a lucrative agglomeration. In 2014, Tencent earned a $3.9 billion profit on $12.8 billion of revenue, numbers slightly better than Facebook’s; those figures were up 53% and 30%, respectively, from 2013, and sales have been growing at a pace that should make Tencent a member of Fortune’s Global 500 by 2018. With headquarters in Shenzhen, across the waters from Hong Kong, Tencent has more than 27,000 employees and $4 billion in cash, and as measured by its market capitalization (which briefly topped $200 billion in April), it’s one of the 40 most valuable companies in the world.

In the first quarter of 2015, online games were responsible for more than 50% of Tencent’s revenues; social networking accounted for about 25%; and less than 15% came from advertising. The company’s roots, though, are in messaging and social media. Back in 1999, Tencent’s instant-messaging service, QQ (an imitation of an Israeli service called ICQ), became an overnight sensation, eventually amassing more than 800 million users. In 2011, Tencent outdid itself with WeChat (Weixin in Chinese), which quickly passed QQ in the app rankings in China.

Today WeChat has half-a-billion users from across China, urban and rural alike, who can post pictures on their Moments page (à la Facebook’s News Feed) or chat in small groups. And with their easy integration of animation and photos, WeChat message streams make Facebook Messenger look Neolithic. But what makes WeChat truly stand out, compared with Facebook and other social networks, is that it has found a way to make its users spend real money—buying stuff from partner companies in which Tencent has a stake, and using Tencent’s own PayPal-like payments method. Social network users routinely reserve taxis on WeChat; order takeout from Tencent-backed Dianping, which lets them scan menus and read restaurant reviews; and then click to shop at Tencent-backed retailer JD.com, Alibaba’s biggest e-commerce rival. In minutes they’ve blown through $50 on cabs, dumplings, and T-shirts—and all the transactions have gone through Tenpay.

For Tencent, this self-contained money flow represents an unequaled revenue opportunity. The amount of mobile payments in China is expected to triple to $3 trillion in 2018 from $1 trillion in 2014, according to iResearch. If Tencent can command even a third of total transactions through its payment platforms and charges a conservative transaction fee, e-payment revenues could easily reach $5 billion a year—more than a third of Tencent’s current revenue. Every relationship with a Line0 or Dianping brings new blocks of people into Tencent’s payments universe. “It’s not just about adding a product or user base,” says a former Tencent developer. “It’s uniting an army.”

That mentality explains why Tencent’s venture capitalism differs so greatly from the American model, where VCs on Sand Hill Road grow rich from their early (some would say lucky) bets on Twitter (TWTR), Facebook, and Google. Instead of trying to pick freestanding winners, Tencent is investing in small companies in the hope that they’ll drive revenue for its core businesses. To get a sense of what Tencent is doing, imagine Elon Musk investing in satellites that need to be shot into space on his SpaceX rockets, or Jeff Bezos investing in diaper makers and toy companies so that they’ll sell more stuff through Amazon.com.

Some of Tencent’s investments in 2014 were big enough to make headlines overseas: The company paid $215 million for a 15% stake in JD.com; an estimated $400 million for 20% of Dianping; $145 million for 10% of online fashion retailer Koudai. But most of its deals were small, focused on startups with little in common other than users who buy things—and buy them often.

Woqu (“I go”) founder and CEO Ivan Huang started an online travel site that offered Chinese customers only one destination: America. “The U.S. is such a big country, we can offer vast products, including flights, car rentals, motor homes,” Huang explains. He has 200 employees in two offices, presided over by a grinning, omnipresent hippopotamus mascot. A mural in the Beijing office shows half-a-dozen hippos exiting a plane into a waiting Woqu-booked limo, checking into a Woqu-reserved hotel, and joining a Woqu-booked tour group. Woqu has 20,000 monthly users and about $3 million a month in sales; the company got $20 million from Tencent and others last year.

In 2013, Yun Tao, a round-faced 29-year-old from China’s Inner Mongolia province who looks like a grownup version of Buzz from Home Alone, started a cleaning service called E Jia Jie. His maids crisscross Beijing with their own solvents, charging rates starting at $4 an hour. Last year E Jia Jie found itself juggling funding offers from both Alibaba and Tencent—“Alibaba wanted to come in at 2 p.m. and sign a contract, knowing that Tencent was scheduled to come in at 4 p.m.,” says Yun—but he eventually accepted Tencent’s $5 million.

Guahao, an online reservation service that helps its 100 million users make appointments in China’s crowded hospitals, received about $100 million from Tencent in 2014. As co-founder Zhang Xiaochun says, meaning it as a compliment, “They leave us alone.” That’s a common theme among Tencent-funded entrepreneurs. Woqu’s Huang went with Tencent because he was convinced it wouldn’t meddle in his business; Yun chose it in part because he had heard from friends that Alibaba made changes at companies it backed.

The theme is surprising because, not long ago, Tencent had a reputation for bullying smaller rivals. In 2010 a Chinese tech magazine featured a satirical depiction of Tencent’s smiling-penguin mascot on its cover, promoting a story that concluded, “They don’t create, just follow suit” (according to a translation). “Two years ago they had a fearsome reputation as being hostile—i.e., [they’d] clone your product and gobble you up alive,” says Rui Ma, an angel investor in China. “They’ve been much more collaborative since then.”

Startup distrust may not have completely evaporated, but observers give a couple of Goldman Sachs (GS) alums credit for working to dispel it. James Mitchell, Tencent’s chief strategy officer, joined the company in 2011 after leading Goldman’s research team in Manhattan analyzing Internet and media companies. When he arrived he didn’t speak the language and wasn’t a China hand, but he brought a banker’s sensibilities for relationships and politics. (He’s also a fast learner: These days Mitchell, a U.K. native, holds forth in Chinese at the monthly strategy meeting.) The company’s soft-spoken president, Martin Lau, is another Goldman veteran from Hong Kong; he arrived in 2005. Former Tencent employees say Mitchell and Lau helped persuade the company’s co-founder and CEO, Ma Huateng (known as Pony Ma), to off-load capital-intensive divisions in search and e-commerce and focus on partnerships.

From Tencent’s perspective, the partner companies don’t even have to be profitable. A case in point is the Uber-like taxi-hailing app Didi Dache, which beams your location to nearby yellow cabs. It is hugely popular, with more than 100 million users, and it raised $700 million last year in a funding round that included Tencent. Still, the business lost tens of millions of dollars in 2014, analysts say, as it offered margin-destroying discounts in a fight for market share against an Alibaba-backed taxi app, Kuaidi Dache.

Those two services ended up merging in February, in a new company that has both Tencent and Aliababa as investors. But by then Tencent already had what it cared about most: millions of new payment accounts from passengers who used Tenpay to transfer money to drivers. Cynthia Meng, an analyst at Jefferies in Hong Kong, says the Didi Dache deal fits Tencent’s modus operandi. “It’s all to potentially convert their existing user base into payments users so they capture the growth of e-commerce,” she says.

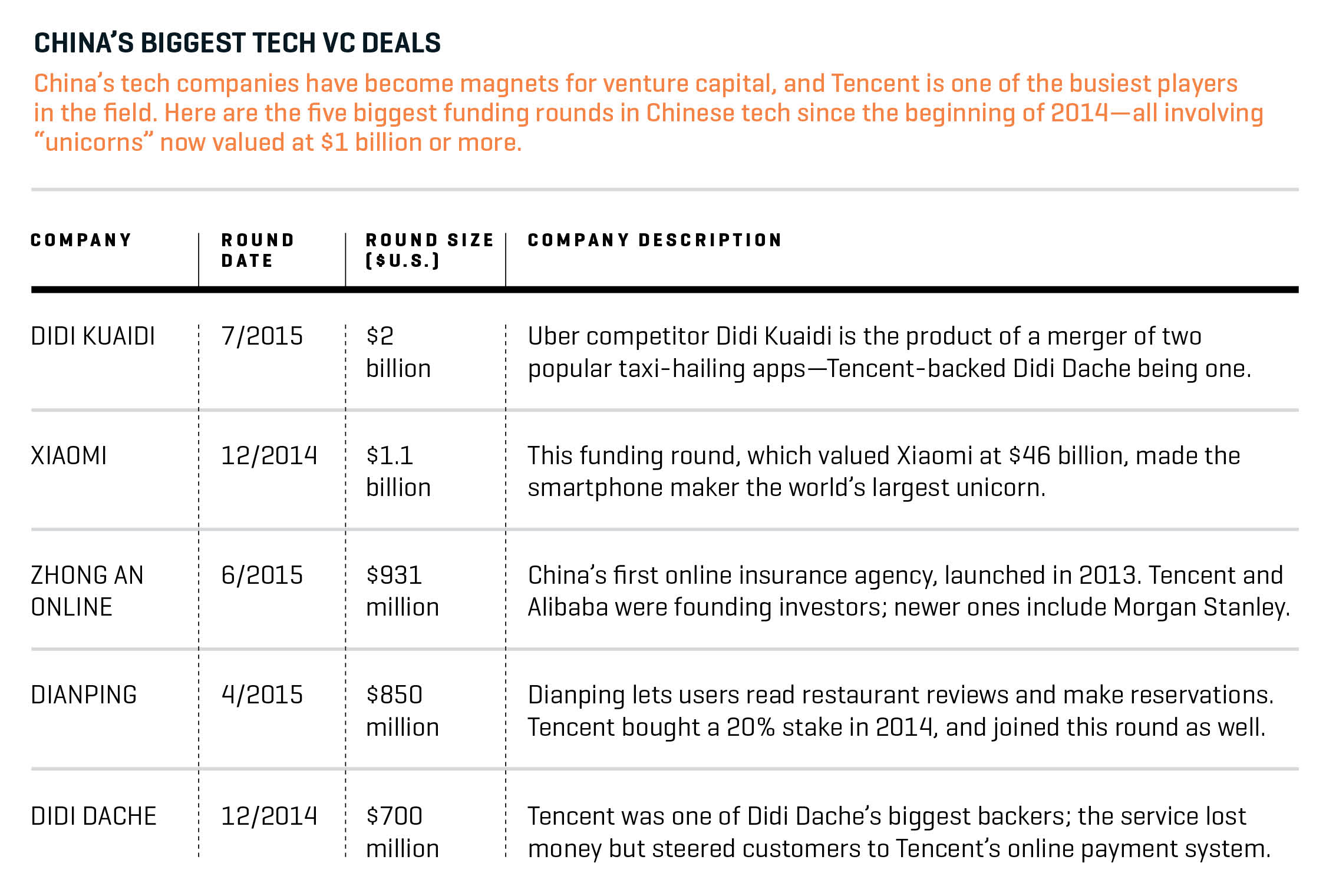

Click chart to enlarge.

Converting shoppers into payment users, of course, is how Tencent’s biggest rival came to dominate China’s mobile-payment market. Alibaba’s Alipay currently has an 80% market share, according to iResearch, and claims about 350 million registered users. Walk down any street in urban China, and you’ll see its logo: The company has forged payment partnerships with brick-and-mortar retailers (including U.S.-based giants Walmart (WMT) and KFC) and dominates “peer-to-peer” transfers, which allow consumers to send money to each other. In June an executive at Alibaba’s payments subsidiary told Fortune, “With Alipay, you could leave the house with just your cellphone and no cash or cards, and chances are you will survive.”

But Alipay’s advantage isn’t insurmountable. The service’s lead is still driven by sales on its shopping sites Taobao and Tmall, which even the most fanatic shoppers use only a couple of times a week. Tencent, in contrast, is building a network of services that could be used more than once a day. And thanks to that network, WeChat is now a backbone for online-to-offline services, a “sector even larger than online shopping” in China, says iResearch analyst Will Tao.

“They’re adding more and more services onto their platform so that people can have a one-stop shop,” says analyst Elinor Leung of CLSA in Hong Kong. Leung estimates that Tencent’s payment network is already worth $20 billion—a tenth of Tencent’s market capitalization—and has the potential to grow a lot more. In an earnings call in May, Tencent president Lau said the payment system creates a virtuous cycle. “You need to have more merchants; then you can actually attract more users,” he said. “And then by having more users, you can actually attract more merchants.”

In January, China’s second-most-powerful Communist, Premier Li Keqiang, traveled to Shenzhen to christen Tencent’s newest creation: WeBank, the country’s first online bank. Li gushed as though China had gone to the moon. “It’s one small step for WeBank, one giant step for financial reform,” he said, surrounded by cheering Tencent employees wearing WeBank T-shirts.

Since China opened to the world in the 1980s, finance has been controlled by a group of stodgy state-owned banks. But regulations are changing fast, and the tech giants are leading the charge. At the moment WeBank is tiny in terms of deposits. (Tencent owns 30% of the venture; it has investment firm partners.) Paired with WeChat payments, however, it has the potential to be enormous: Imagine Apple (AAPL) syncing Apple Pay with an Apple bank.

WeBank will bring in deposits and could offer loans to boost the services WeChat users are flocking to. And Tencent has other finance experiments on the drawing board. Bitauto, a Chinese online car-listing portal that trades on the NYSE, received a $1.5 billion joint investment from JD.com and Tencent in January; Bitauto is now exploring ways to derive a customer’s credit rating from WeChat activity, eliminating the need for a formal credit report. Bitauto CEO William Li says Tencent offers what China’s other tech giants can’t. “You can buy expensive search placement on Baidu, so a partnership is not necessary. Alibaba is just a marketplace,” Li says. “But Tencent—it wants to connect services.”

Credit ratings and car loans may seem like a stretch for a social-networking and online-games company. But, of course, so do maids on motor scooters, hospital patients, and globe-trotting hippopotami—all of which already fit under Tencent’s venture capital umbrella. The network of services keeps growing. Now Tencent needs to make sure Tenpay makes it profitable.

A version of this article appears in the August 1, 2015 issue of Fortune magazine with the headline “Tencent grows its own economy.”