The announcement that Verizon is buying AOL has the financial media buzzing more for what it says about the future of the media and telecom businesses than for the pure size of the deal.

After all, as my colleague Geoff Smith noted this morning, the $4.4 billion Verizon (VZ) is paying for AOL (AOL) amounts to “loose change” for the nation’s largest wireless provider.

At the same time, it does offer the opportunity to check in on the M&A market in 2015, which has been active and looks like it will heat up even more as the year goes on.

According to Dealogic, the total volume of global mergers and acquisition volume came in at roughly $3.5 trillion in 2014 — beating the 2013 totals by a healthy 26%. Total deal volumes in 2015 are at $1.4 trillion including Verizon’s acquisition of AOL. That’s the fastest pace we’ve seen since 2007, and if the wheeling and dealing keeps up at this rate, the total number of deals could outstrip every year on record other than 2007.

There are several reasons for the boom. Stock markets are getting pricey, giving executives plenty of firepower to finalize deals. At the same time, interest rates are at record lows, making deals like Verizon’s–which was funded with commercial paper–relatively inexpensive. Meanwhile, corporate executives are facing slow-growing markets in the rich world, with apparently few opportunities to invest in their own operations to create shareholder value. So, the next best option is to buy someone else’s operations.

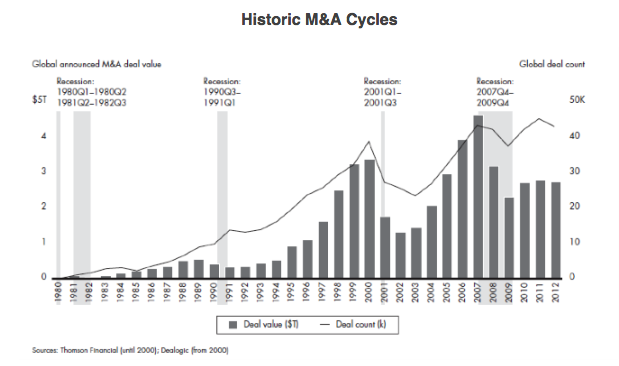

Whether or not you agree with this particular management strategy, examining the M&A cycle can tell us something about the economy in general. Take a look at this chart from Generational Equity, which shows the M&A cycle going back to 1980:

M&A activity tends to peak in the year or two before the economy contracts (recessions are indicated by the shaded areas in the chart). Given that 2015 deal volume is on pace to surpass 2014 figures by about 11%, one might get worried that M&A levels are reaching a danger zone, signaling a coming stock market bubble and possible recession.

But another point to take from the above chart is that M&A volumes have surpassed previous peaks before each of the past three recessions. It still doesn’t appear as if M&A is on pace to surpass the 2007 record of $4.6 trillion in deals. Of course that may change, with big deals rumored, like the $40 billion hostile offer that pharmaceutical firm Teva made to Mylan (which is in turn offering nearly $30 billion for Perrigo) last month. But for the time being, it looks like the M&A market has a few more years to ramp up before the next recession. That’s good news, considering our current economic expansion is one of the longest running on record. But it pays to keep track of these trends, as it may just help you spot the next serious downturn.