It’s not everyday that a nascent industry gets the endorsement of a figure as prominent and well respected as Larry Summers.

The former Treasury Secretary and world-famous economist has, however, made the online lending industry one of his pet projects since leaving the Obama Administration. He now sits on the board of the Lending Club, America’s largest peer-to-peer lender as well Square Capital, the lending arm of payments company Square.

On Wednesday, he delivered the keynote address at the conference Lend It 2015, outlining the reasons why the industry excites him and why he believes “technology based businesses have the opportunity to transform finance over the next generation,” and do so in a way that makes the economy more efficient and stable.

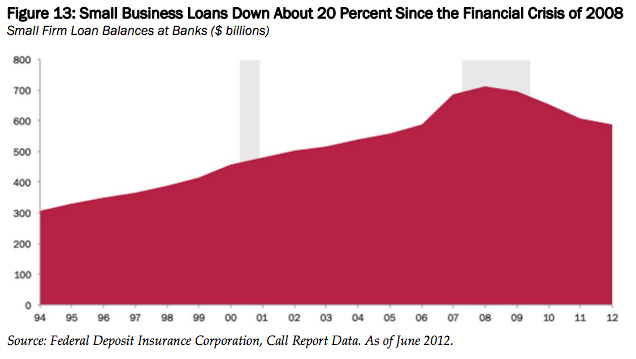

Online lending in recent years has gotten a reputation as a good alternative for consumers with good credit who want to consolidate credit card loans at much lower rates. But Summers sees great potential for online lending in the small business sphere. His colleague at Harvard, former Small Business Administrator Karen Mills–also a speaker at the conference–provided some numbers from her research that showed just how badly innovation is needed in this area. The following chart shows how small business lending has declined since 2008, and has yet to recover:

And since 2012, lending has basically remained flat. This is in an economy where, according to Mills, half of all workers own or work for small businesses. In so many ways, be it total number of jobs, or total output, the economy has recovered, yet lending to the engine of job growth in America has lagged. One reason for this is that rapid consolidation happening in community banks, the firms most responsible and able to make small loans to small businesses.

What excited folks like Mills and Summers about online lending is that companies from Paypal to Square are able to use their existing base of small business customers, and the bevy of information they have about them, to make smart lending decisions in a way that makes borrowing simple and flexible for small businesses. Online lending only counts for about $10 billion of $700 billion in outstanding loans, but the following chart shows how online lenders are growing quite fast, even as banks retreat from the market:

It’s this dynamic that has folks like Summers truly excited about online lending. On Wednesday, he agreed with former Fed Chair Paul Volcker when Volcker said that the only useful innovation in finance in the past generation has been the ATM. Finance has innovated, but the benefits of these innovations have gone to large capital holders and not society more broadly.

With online lending, Summers argued, the information available the information made available makes it easier for borrowers and lenders to make good decisions and will drive up profits for lenders and costs down for borrowers, all the while extending credit to small businesses that banks can’t afford to consider lending to because they have less information at their disposal and higher cost structures. It’s this logic that leads Summers to believe that online lenders could eventually capture upwards of 70% of the market share in small business lending, and why a Wall Street bigwig like Jamie Dimon said in a recent letter to shareholders that “Silicon Valley is coming” after the banking industry.