The most feared man in corporate America these days is not named Icahn, Ackman, Loeb, or Einhorn, but rather Smith, as in Jeff Smith, the boyish-looking 42-year-old co-founder and CEO of a previously obscure $3 billion activist hedge fund called Starboard Value. In October, Smith accomplished something that even his more flamboyant, better-known activist peers can’t boast about: He took effective control of a Fortune 500 company—Darden Restaurants, the owner of Olive Garden and Longhorn Steakhouse, which ranked No. 319, with some $8.5 billion in sales last year—while owning less than 10% of the company. Thanks to his success in running a highly contested proxy contest, Smith replaced the entire 12-member board of directors and assumed the role of chairman. Along with his handpicked board, he will soon choose a new CEO to run Darden. Welcome to the new world of corporate takeovers.

Smith is well aware that his stunning victory represents a landmark moment in a long-running debate: What is the correct balance of control over publicly traded companies between management and shareholders? After a brilliantly executed campaign that included both withering public criticism of Darden’s (DRI) leadership and careful courtship of the company’s other major shareholders, Smith now professes that his focus is on improving the performance of Darden, not celebrating his coup. But he also knows that he has fired a shot over the bow of directors everywhere. Shareholders, particularly noisy ones running activist hedge funds, are ascendant—and managers ignore them at their peril. “It was really amazing how many people reached out to me in the days following to say that they had a conversation with a CEO who said, ‘The world has just changed,’ ” says Smith.

There is little question anymore that activist investors have become a powerful force across corporate America, driving changes not only in boardrooms but also in executive suites. The old master of the game, Carl Icahn, 78, has become the richest man on Wall Street, with an estimated fortune of some $24 billion, by tactically applying pressure on CEOs to extract, say, stock buybacks and a couple of seats on the board, then selling his stake for a handsome profit. And in the years following the financial crisis, a host of agitators have followed his example. Since the end of 2009, according to Hedge Fund Research, the amount of money in activist hedge funds has jumped from $36 billion to $112 billion. Activists such as Bill Ackman of Pershing Square Capital, Greenlight Capital’s David Einhorn, and Dan Loeb of Third Point have become adept at the art of shaking things up. (See “Activist investors: The best (and worst) performers of 2014” for more on recent activist campaigns.) But the scope of Smith’s triumph with Darden has left jaws hanging open across Wall Street and beyond. Only in a handful of times in the past few years has an activist managed to replace an entire board of directors, and never at a company the size of Darden.

The story of how Starboard outmaneuvered Darden’s leadership is a cautionary tale for managers and directors everywhere. The board that Smith went up against was chock-full of talent and experience. Among them were longtime CEOs, investment bankers, a former U.S. senator, a business school professor, and senior executives at Wal-Mart and Gannett. Both the board and the company were advised by Wall Street’s best—including Goldman Sachs, Morgan Stanley, and Wachtell Lipton, the powerful law firm. Yet they played into Smith’s hands at every turn. For example, when Smith publicly blistered Darden for selling its struggling Red Lobster seafood chain, the directors privately scoffed at his analysis but refused to hold a special meeting with shareholders—alienating other investors in the process. Eventually, at the proxy vote on Oct. 10, frustrated Darden shareholders such as Capital Research and Management, which owns around 11.5% of Darden, and Vanguard Group, which owns around 7%, handed an overwhelming victory to Smith. “They were blind to how their actions were going to directly lead to this result,” says Smith of the old board. “It’s kind of surprising.”

No doubt the directors felt blindsided. Steve Odland, the CEO of the Committee on Economic Development and a former CEO of Office Depot, was nominated to be a new independent board member at Darden in the months before the October shareholder vote. Like the other directors proposed by Darden in a last-ditch effort to reach a compromise with Smith, Odland lost. He empathizes with the ousted Darden directors. “My sense from having met the Darden board members is that they’re very highly qualified people,” he explains. “As I look at it, I say, ‘Gee, this could happen to any board.’ These people had followed everything that was good governance and done what they were supposed to do, and it happened to them.”

Starboard wasn’t the first hedge fund to spot weakness at Darden. The activist assault actually began in June 2013, when Barington Capital Group started buying shares in the company and offered its view with management that Darden could increase its stock price by cutting costs to bring its expenses more in line with its peers. That September, Barington wrote a letter to Darden’s board recommending that Darden form two independently managed restaurant companies: one made up of the slower-growing chains, Olive Garden and Red Lobster, the other comprising Darden’s faster-growing restaurants, such as Capital Grille, Yard House, Eddie V’s Prime Seafood, Seasons 52, and Bahama Breeze. Barington also wanted Darden to consider putting its extensive real estate holdings—1,048 properties and another 802 ground leases—into a publicly traded real estate investment trust, or REIT. Barington argued that those steps would increase Darden’s stock to between $69 and $76 per share, far above its then price of $46. A few weeks later Barington publicly announced that its investor group had accumulated a 2.8% stake in Darden and reiterated the split-up plan.

Before it was a public company, Darden was a group of restaurant brands tucked inside food giant General Mills. At the urging of, among others, then General Mills board member Michael Rose, a former CEO of Harrah’s Entertainment, the conglomerate spun off Darden in 1995. Rose joined the Darden board and remained on it until after Smith’s coup d’état. Clarence Otis, a former investment banker at Kidder Peabody, became CEO of Darden in November 2004 and presided over seven years of nearly continuous growth. Thanks to acquisitions and internal growth, revenue increased to $7.5 billion in 2011 from $5 billion in 2004. “The stock was up 900% in 19 years,” says Rose of his full tenure on the board. “That’s really good performance over a long period of time.”

But by 2012, Darden’s growth was hitting a wall. Same-store sales at Olive Garden, Red Lobster, and Longhorn Steakhouse had begun to stall in the years after the financial crisis as the lingering recession hit the company’s middle-class customers with full force. After a respectable financial performance in 2012 and revenue gains across the board, at the end of the year Darden announced downward revisions to its expected fiscal year 2013 results. The stock tumbled. And the following year was indeed brutal for Darden. Although revenue at Olive Garden increased by $100 million in 2013, to $3.7 billion, its same-store sales fell 1.5%. Most of the increase in revenue had come from higher menu prices. At Red Lobster year-over-year revenue actually decreased $50 million, to $2.6 billion. The company’s smaller, faster-growing chains continued to perform fine, but Darden’s overall Ebitda—a measure of earnings key to assessing a company’s health—fell to $1.043 billion, from $1.089 billion in 2012. That was not the financial performance that Wall Street expected. Over the three years through the end of 2013, Darden’s stock gave shareholders a total return of 31%, vs. 56% for the S&P 500.

The Darden board knew that Red Lobster had become a problem, and management believed that it would be difficult to fix. “We had a company—Red Lobster—that had been facing tough times,” says William Lewis, a managing director at advisory firm Lazard and a longtime Darden board member. “I mean, we had been dealing with this in the boardroom for six or seven years.” Still, the market and the media could smell blood. “Darden needs shaking up, and a split could be a logical move,” Barron’s concluded on Nov. 30, 2013.

On Dec. 17, Barington unloaded on Darden, using what has become standard practice among activist hedge fund managers: the shock-and-awe PowerPoint presentation. In its 85-page document, released publicly, Barington reiterated much of what it had already told Darden’s leadership team. The company had underperformed its peers in nearly every way, from same-store sales growth to stock performance. Barington said its reorganization plan would now create more value for shareholders than it had outlined previously: a range of value between $71 and $80 per share was in the offing. “We believe Darden is undervalued and has the potential to deliver materially stronger returns for its shareholders,” Barington argued.

Two days later Darden reacted to Barington’s six-month assault with its own plan either to sell or to spin off Red Lobster, to cut capital expenditures by $100 million, and to reduce costs by some $60 million annually. Darden said it would maintain its attractive quarterly dividend of 55¢ a share and would continue its plan to buy back stock, which, along with the dividends, had returned more than $1.3 billion to shareholders over three years. “After thorough and extensive consideration, we have decided that the actions announced today best position us to enhance value for our shareholders,” Otis said. Darden’s stock fell about 5% on the news.

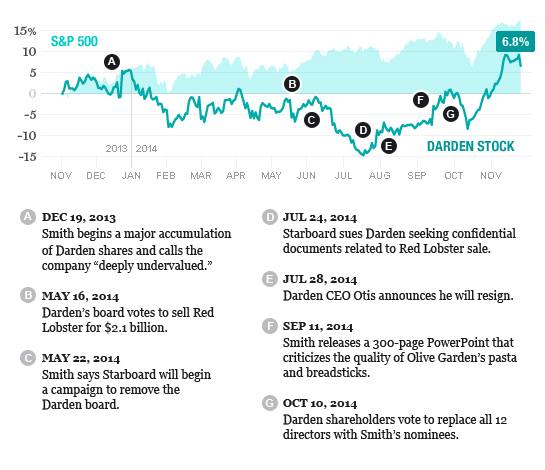

Smith smelled an opportunity. His various Starboard funds had been buying and selling Darden stock sporadically, but after Darden’s announcement on Dec. 19, Starboard started a major accumulation that totaled 7.25 million shares, or 5.6% of the stock. Smith filed Starboard’s 13-D on Dec. 20. He thought Darden’s plan stank, and said so. He said that Darden was “deeply undervalued” and that “Starboard believes that the plan outlined by management falls significantly short of the actions required to maximize shareholder value.” He agreed with Barington that Darden’s real estate holdings should be put in a separate, publicly traded REIT. “Starboard may make recommendations regarding corporate strategy, capital allocation, financial performance, and board composition,” Smith wrote. The stock spiked.

But joining the fight with Darden was more than just a moneymaking opportunity for Smith. It was a chance to burnish his brand as an activist investor. He had already earned a reputation among fellow activists as having a talent for shaking up corporate boardrooms. “Starboard has certainly become one of the main go-to firms in activist situations,” says Sahm Adrangi, the chief investment officer at hedge fund Kerrisdale Capital. But even some of his fans felt that Smith had something to prove. “I would put him in the ‘arrogant punk’ category,” says one hedge fund manager who has joined Smith’s activist campaigns in the past.

Smith grew up in Great Neck, Long Island, a suburb just east of New York City that is also the birthplace of Steven A. Cohen, the infamous hedge fund manager. Smith’s mother was a real estate broker, and his father was the founder of the Fresh Juice Co. After graduating from the Wharton School at the University of Pennsylvania in 1994 with a degree in economics, Smith worked in the fledgling M&A department of the big French bank Société Générale. From there Smith headed to his father’s company as vice president of strategic development and a member of the board. In 1998, at the younger Smith’s initiation, the Smiths sold Fresh Juice to Saratoga Beverage for around $20 million. Jeff Smith then moved to Ramius Capital, a small hedge fund and private equity firm started by Peter Cohen, a former CEO of Shearson American Express. At Ramius, Smith made direct investments in small, publicly traded companies and ran an internal hedge fund. After the financial crisis in 2008, Ramius merged with Cowen Group, an investment-banking firm that was once part of Société Générale. In 2011, Smith and two of his partners spun Starboard out of Cowen.

Starboard started small in activism before working its way up to the big Darden fight. In 2011, Starboard won board seats on SurModics, a biopharmaceutical company, and on Regis, the nation’s largest operator of hair-cutting salons and the owner of Hair Club for Men. In December 2011, Smith took on a bigger target when he went after online media company AOL. He accused CEO Tim Armstrong of wasting money by funding the losses at Patch, a network of local-news websites. Smith wanted seats on the AOL board but lost a proxy battle in June 2012—one of his few defeats. Still, he won the AOL war. Armstrong ultimately spun off Patch. And, as Smith advocated, AOL agreed to return to shareholders much of the more than $1 billion it received from the sale of its patents to Microsoft in 2012. Starboard, which had accumulated a 5.3% stake in AOL, saw the value of its AOL stock soar by about 250%.

Smith’s next corporate target was Office Depot, in which he eventually accumulated a 15% stake. He wanted CEO Neil Austrian removed, and he pushed for the completion of Office Depot’s already announced merger with Office Max. Smith also wanted to appoint a majority of the board. In the end, Office Depot reached a compromise with Smith and awarded Starboard three board seats. Smith has also taken activist positions in Smithfield Foods, Calgon Carbon, and Tessera Technologies. According to Institutional Investor, the Starboard team has generated annualized returns of 15.5% since the inception of the activist fund at Ramius in 2002 through May 2014 and has made money in 84% of its activist campaigns. Since 2004—not including Darden—Starboard has replaced some 80 directors on about 30 corporate boards.

ANATOMY OF AN ACTIVIST CAMPAIGN

Unlike the board of Office Depot, Darden’s directors were not in a compromising mood when Smith came calling. Lazard’s Lewis says that the idea that Barington and Starboard suggested anything that the Darden board wasn’t already aware of was laughable. “We systematically analyzed everything that they suggested and more,” he says. Lewis points out that he, along with fellow board members Mike Rose and Charles Ledsinger, the founder of Sunbridge Capital Management, had years of real estate experience. “Their thoughts about ways to unlock value made the Starboard stuff look like grade-school work,” one board member says. “There was just no way to, in our judgment, based on all the work we did, give merit to any of their arguments.” Darden had already engaged Goldman Sachs to begin the sale process for Red Lobster and had appointed a four-member subcommittee of the board—comprising Lewis, Ledsinger, Rose, and Victoria Harker, the CFO of Gannett—to oversee the process. Goldman contacted more than 70 potential buyers of Red Lobster and another 25 potential buyers of the real estate related to the chain.

Starboard, however, was not impressed by the Darden board’s actions. After speaking with Otis and several of the other Darden senior managers on Jan. 8, 2014, Smith wrote the CEO a five-page letter two weeks later and copied the board. He also released the letter publicly. In it, he reiterated his view that spinning off Red Lobster as its own publicly traded company was a terrible idea (no mention was made of the option to sell Red Lobster to a third party) and that Darden needed to explore the REIT option. He also returned to the idea of splitting Darden into two companies.

On Jan. 29 the management team met with Starboard at Darden’s flashy headquarters in Orlando. At the meeting Darden executives said they still planned to move forward with the spinoff or sale of Red Lobster. Again, Smith objected. In a Feb. 10 letter, also released publicly, he wrote he was “surprised and terribly disappointed” by the management’s willingness to move ahead with the sale, which was indicative of the board’s intention to ignore the “serious concerns” voiced by Darden’s shareholders about “the potential destruction of shareholder value.” Smith also wrote that he had been in touch with Darden’s other large shareholders, and they shared his negative view about the sale or spinoff of Red Lobster. He then threatened to mount a proxy fight to replace a majority of the board members at the 2014 annual meeting in September.

It was becoming painfully obvious that the two sides were dug into their positions. On Feb. 24, Starboard filed a preliminary solicitation statement seeking to get a majority of shareholders to vote to hold a special meeting to try to thwart the sale of Red Lobster. Any vote held at the special meeting would be non-binding, and as Wachtell Lipton no doubt made clear, the Darden board was well within its legal rights to sell the business without shareholder approval. But the message from shareholders would be resounding. Whether the board would hear it was another matter.

The prospect of a shareholder vote on the Red Lobster sale had an understandably chilling effect on the sale process Goldman was running. Potential bidders complained to Goldman, according to SEC filings, that “the uncertainty associated with a shareholder approval closing condition would be unacceptable.” The very idea that shareholders might call a special meeting to register their displeasure with the sale was having the effect Starboard wanted. But Darden and its board continued to plow ahead. On March 10, Darden filed a registration statement with the SEC to begin the process of spinning off Red Lobster, if that proved to be the preferred alternative.

Later in March the Darden board met for two days to hear about the status of the various options being considered for Red Lobster. At the meeting the board also enacted changes to its bylaws that many viewed as hostile to shareholders: It delayed the annual meeting and made it tougher for shareholders to make changes. The board claimed the moves were in keeping with what other companies do. The activists and shareholder-rights organizations, such as Glass Lewis and ISS, were aghast. “One has to wonder why the board chose this particular time to ‘modernize’ the bylaws by granting itself powers to obstruct, or otherwise raising defenses against, shareholders who might wish to use the annual meeting to hold directors accountable,” ISS later observed. (ISS did not respond to a request for comment, and Glass Lewis declined to comment for this article.) On March 21, Darden management shortened its quarterly earnings call to 45 minutes. The analyst and investor meeting scheduled for March 28 was canceled. In response, on March 31, Starboard trotted out a 207-slide PowerPoint presentation making a detailed case for the special meeting.

By this time, Darden board members suspected that Smith had enlisted the support of Darden’s other big shareholders, particularly that of Greg Wendt, the San Francisco–based manager of a fund at Capital Research, Darden’s largest shareholder and not a firm known for being activist. “It was very clear that they were working hand and glove with Starboard,” says one former Darden board member. (A spokesman for Capital Research says it is the company’s policy not to comment publicly about its investments.) Former longtime Darden board member Mike Rose says Starboard developed a symbiotic relationship with the big institutional shareholders such as Capital Research. “If Capital Re is unhappy, Capital Re is not about to call up Fidelity and say, ‘We are unhappy,’ because, first of all, they are competitors and, second of all, because that starts to violate SEC rules,” he says. “They start to act as a group when they do that. That requires filings. So Capital Re can talk to Starboard and Starboard can talk to Fidelity, and it’s the same thing.”

On April 22, during the Active Passive Investor Summit in New York, Smith appeared on CNBC. He said the spinoff of Red Lobster could cost shareholders as much as $1.6 billion, between the lower multiple that he expected an independent Red Lobster to trade at and his belief that $800 million in real estate would be “trapped” there. He said Red Lobster was struggling with high seafood prices and low customer volumes and should be kept by Darden until a comprehensive strategic plan could be enacted. Asked whether Clarence Otis should be removed as CEO, Smith said, “Is Mr. Otis in a hot seat? I think he is in a hot seat.” Later that day CNBC reported that Starboard had won 54% of the vote of Darden shareholders to hold a special meeting, which Darden was now compelled to do within 60 days. (In the end Starboard won 57% of the vote.)

Final bids for Red Lobster came in toward the end of April, and the board’s special committee huddled with Goldman and Morgan Stanley for the first few weeks of May deciding what to do. It turned out there was only one serious bidder for Red Lobster: Golden Gate Capital, a San Francisco–based private equity firm with $12 billion under management and the owner or former owner of such diverse businesses as California Pizza Kitchen, Ann Taylor, Eddie Bauer, and Pacific Sunwear.

On May 14, Smith appeared at the SALT hedge fund conference in Las Vegas on a panel about activist investors. He made the revealing point—as Darden board members were all too aware—that the current age of activist investing had solidified the bonds between activist investors and traditional institutional investors. “The institutional-shareholder base actually knows us collectively as activist investors far better than any one management team,” he said. “And frankly trusts us more. That’s a big divergence than where it was five years ago, 10 years ago, 15 years ago.” As for Darden in particular, Smith estimated that his real estate plan for the company would unlock another $10 per share, and his plan to improve operating margins—which he said were 250 basis points below industry averages—would create another $10 per share in value. “There’s tremendous opportunity at Darden,” he said. What he was having trouble fathoming is why the board and company were being so intransigent. He said the spinoff or sale of Red Lobster was an “irrational” act.

Just a couple of days later, on May 16, despite Starboard’s victory in the vote for a special meeting, the Darden board voted unanimously to sell Red Lobster to Golden Gate for $2.113 billion in cash, a multiple of nine times trailing 12-month Ebitda. It was “a fucking great price,” one board member says. Mike Rose says Golden Gate’s purchase price was “$300 million more than our target price.” After paying a capital gains tax of about $500 million, Darden intended to use $1 billion of the remaining proceeds to pay down debt and the balance to buy back its stock. Rose says the advisers told the board that if it postponed the sale, they didn’t think the buyer would be there, or the price would come down significantly. “So the board, I think, did the absolutely right thing,” he says. Darden also said it would file a proxy statement to begin the process of holding the special shareholder meeting as required, even though it was a moot point. A few days later, Smith wrote that the move “simply adds insult to injury.” Analysts seemed to agree with him. “Who Knew Lobsters Had Middle Fingers?” was the title of a research report by Mark Kalinowski at Janney Capital Markets.

Smith was incensed. “The announced sale woefully undervalues Red Lobster and its real estate assets,” he said in a statement at the time. He wrote in a subsequent letter to shareholders that the Red Lobster sale was a mere $100 million more than Starboard had valued Red Lobster’s real estate alone, “implying that Darden is essentially giving away the Red Lobster operating business, an iconic brand with $2.5 billion in sales, for less than 1x Ebitda.”

Rose says the board strongly disagreed with Starboard’s analysis but felt its hands were tied on the PR front. “As board members, we took into account the long-term best interest of our shareholders, even though our shareholders really didn’t understand that it was in their best interest, and we couldn’t really tell them because we couldn’t communicate how bad Red Lobster was performing without screwing up our sale,” he says. “And so we made a very difficult decision. We went ahead with the sale, and from that day on, the handwriting was on the wall that we were going to lose the entire board.” The directors were like “the folks at the Alamo,” says Rose. “We knew what was coming, but we decided to fight until the bitter end rather than give up.”

Smith readied an all-out assault. In a 20-page letter to his fellow shareholders on May 22, Smith announced that Starboard would begin a proxy fight to remove the Darden board. He also said that Starboard had increased its ownership of the company to 6.2%. (Ultimately Starboard would end up with 8.8% of Darden’s shares.) Smith wrote that the board’s claim that it had sold Red Lobster for nine times Ebitda was yet another example of the board’s and Darden management’s “fundamental lack of understanding” of Red Lobster’s assets and their “predilection” to “mislead” shareholders. Golden Gate Capital had gotten Red Lobster for a bargain price, Smith claimed. He wanted the full board replaced and named his 12 board nominees, including himself and one of his partners.

The fight between Smith and the Darden board was verging on a holy war by now. Wendt of Capital Research told the directors that the fight had gone beyond a difference of opinion on strategy, recalls one board member. “He said, ‘The shareholders asked for a vote, and you told them to go fuck off. And that, to us, is theology.’ ” But the Darden board was unmoved by Starboard’s plan. “We were like, ‘We’re the board. We know more than you do. We have more information. We have the best advisers,’ ” recalls a board member. And he says the board would make the same decisions again. “If there was a headline, it would be, ‘We were right. You are wrong.’ ”

During the summer and fall, the parrying between Darden and Starboard continued. On July 24, Starboard sued Darden in Florida, seeking access to confidential documents related to the sale of Red Lobster. Four days later Darden completed the sale of Red Lobster to Golden Gate and announced that Otis would step down as chairman and CEO. Darden also announced that Charles Ledsinger would be the new board chairman and that the roles of chairman and CEO would be split. Furthermore, in an effort—finally—to compromise with Smith, who was expected to easily win the proxy fight, Darden proposed a slate of only nine directors, implying that Starboard could appoint the other three.

Smith, however, demanded more representation on the board. And the two sides went back and forth arguing over the number of seats, with Wendt of Capital Research acting as an intermediary. The board’s attempts to negotiate only spurred Smith on. For instance, after Smith suggested a fifty-fifty board split, the board said it would think about it. Recalls one board member: “When we got back to him to say, ‘Okay, that might make some sense,’ he was like, ‘Nope. That offer is gone, but what about this offer?’ ” Later Wendt told the board that Smith would accept eight of the 12 seats. The majority of the directors voted for the compromise and informed Wendt it would take the deal. But when Wendt called back, recalls this board member, he said, “ ‘Sorry, he won’t do that anymore.’ And so then we realized that Capital Re was also getting played by Jeff Smith.” Smith, for his part, says the board handled the negotiations poorly. “They always wanted a proposal that was proposed a month earlier under different conditions,” he says.

At one point the sparring became comical. Tucked deep inside Starboard’s nearly 300-page PowerPoint presentation on Sept. 11 was a gem about Olive Garden’s ongoing failure to salt the water used to cook its pasta. “Shockingly, Olive Garden no longer salts the water it uses to boil the pasta, merely to get a longer warranty on its pots,” Starboard wrote. “We believe this results in a mushy, unappealing product that is well below competitors’ quality despite similar cost.” Smith also wrote that Darden could save between $4 million and $5 million a year on the cost of bread sticks—Olive Garden serves nearly 700 million bread sticks a year—and that they had lost their taste. Smith compared them to “hot dog buns.” At that point the Starboard vs. Darden fight went viral. HBO’s John Oliver did a three-minute takedown of the presentation on his show, Last Week Tonight, that has now been viewed nearly 700,000 times on YouTube.

When Darden responded to the bread stick PowerPoint soon after with a 24-page “Renaissance Plan” about why shareholders should stay the course, it was too little too late, despite the support the Darden plan received from some research analysts. The vast majority of Darden’s long-term shareholders had had enough. Both ISS and Glass Lewis urged investors to vote for Smith, making the actual Oct. 10 vote a foregone conclusion: Shareholders voted overwhelmingly for Smith and his slate of 12 directors.

Smith wasted little time in taking control. On Oct. 13 he cut a deal with Gene Lee, the Darden president, to become the interim CEO, making effective immediately Otis’s previously announced departure. Smith also threatened not to pay the fees of Goldman, Morgan Stanley, and Wachtell Lipton, but then thought better of it, since the fees were contractual obligations. On Nov. 18, Lee announced a plan that would save Darden about $20 million a year in costs by eliminating a level of senior management and by cutting Darden’s private-jet operations and selling its corporate jet. Through the end of November, Darden’s stock was up about 20% since Smith took control of the company.

While unapologetic about the board’s decisions, former director Rose acknowledges that the directors did not communicate effectively enough with the company’s large shareholders. With better counsel from their highly paid advisers, he says, they might not have lost out to Smith so absolutely. Bankers across Wall Street are conducting a thorough postmortem of what went wrong. Says Rose: “The next time a set of circumstances like this comes around, believe me, all the advisers are going to say, ‘This could turn out like the Darden case, and you need to take that into consideration.’ ”

For his part, former director Lewis acknowledges Smith’s skill as an activist. “I give Smith a lot of credit for his tactics, his ability to tell stories, his ability to connect with the shareholders,” he says. “As an activist, he was brilliant.” However, board members felt that Smith viewed the battle for Darden as less about fixing the company and more about résumé building. “We all very quickly realized that this was his audition for the big stage,” one says. The Darden directors learned lessons about the need for boards to hear directly from a company’s biggest shareholders, free of management filters. “It’s a war,” says one member of the board. “It’s a war. And so you don’t stop. You just keep talking. What are the lessons? Take control of your story. Don’t let someone else take control of your story.”

The fact that Smith now controls the entire Darden board is disturbing to some. Odland, the former CEO of Office Depot who was nominated to be a Darden director, sees a bad precedent. “As a CEO, if I had put 11 of my friends on the board and said, ‘In order for you to come on the board, you must sign up for my plan and agree to that and then we’re going to take out the management together,’ I think that would have been decried as really bad corporate governance by the governance community,” he says. “And yet, in fact, that’s what happened here, and it’s being lauded as good corporate governance.” That’s not to say that Darden can’t be better run, says Odland, or that the board didn’t make mistakes. But the pendulum could swing too far toward activists. Says Odland: “What I worry about with the state of activism is that, in fact, corporate governance has gone from one set of people dominating a boardroom with very little objectivity to another set. And both extremes can be equally as bad.”

Smith dismisses those criticisms as misguided gripes. He says the new board is “infinitely better” than the prior one and that working with activists should be simple for a board. “All you have to do is what’s right for the company and for value,” he says. “That’s it. Listen to your shareholders. They likely have good ideas, and they’re the owners of the business.” He says that his new board is working well with management and that he is “pleased with the attitude, energy, and teamwork inside the company.”

Meanwhile, Smith has moved on to a new challenge. On Sept. 26, before the ink was dry on the Darden proxy fight, Smith sent a letter to Marissa Mayer, the CEO of web giant Yahoo. Two years ago Third Point’s Dan Loeb had pressed his ideas for Yahoo on the company and had come away with little to show for it—other than installing Mayer as CEO and the more than $1 billion in profit he made on Yahoo stock. Now it’s Smith’s turn. He owns less than 1% of Yahoo, but wants Mayer to sell Yahoo’s stakes in Alibaba and Yahoo Japan, to cut costs by as much as $500 million a year, and to stop buying tech startups that don’t add to earnings. He would also like Yahoo to merge with his old nemesis AOL, “a company we know well,” as Smith wrote. On Nov. 14, Smith reported in an SEC filing that he had bought back into AOL, with a 2.4% stake. Fasten your seat belts.

William D. Cohan is a regular contributor to Vanity Fair. His most recent book is the Price of Silence: The Duke Lacrosse Scandal, the Power of the Elite, and the Corruption of Our Great Universities.

This story is from the December 22, 2014 issue of Fortune.