One of the stories that firms deserting our country like to tell is that by moving their corporate domicile (but not their actual headquarters) outside the United States to duck taxes, they will be able to use cash they currently have parked offshore to expand their operations in the U.S.

So when the new rules the Treasury issued in September upended the biggest proposed corporate “inversion” in history—Illinois-based AbbVie’s (ABBV) $54 billion takeover of Ireland-based Shire—there was whining about how the Treasury is killing prospective American jobs.

To which I say: give me a break. Under current law, it’s already relatively simple, inexpensive, and profitable for an American company to use its offshore cash for productive and job-adding U.S. projects. And as I think you’ll see, the method we’re talking about, which Standard & Poor’s has dubbed “synthetic cash repatriation,” looks like a better long-term deal for shareholders than paying a multi-billion-dollar premium to buy an offshore company in an inversion deal.

In an inversion, a U.S. company buys a foreign company, technically sells out to it, and thus transforms itself into a non-U.S. company to avoid high U.S. taxes, but continues to benefit from being in our country. That’s why I (and subsequently President Obama) have taken to calling these inverters “deserters.”

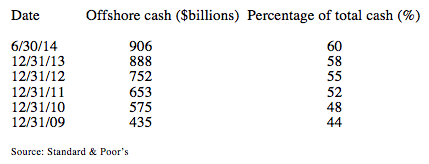

U.S. companies rarely bring home the profits they earn in other countries, because that would subject them to the 35% U.S. corporate income tax, less the tax (if any) paid where the money was earned. As of June 30, S&P estimates that the U.S. companies whose credit it rates held $906 billion of cash offshore, money that would be subject to U.S. tax if companies brought it home directly.

But there’s a simple and obvious way for companies to use the cash indirectly to fund U.S. investments. Think of it as “clever borrowing.”

Here’s how it would work. It’s a play in three acts.

Act One We start with something I learned from tax expert Edward Kleinbard, a University of Southern California law school professor and a prolific, witty, and effective polemicist whose new book, We Are Better than This: How Government Should Spend Our Money, is a must-read for anyone who wants to be educated about taxes and social policy.

Kleinbard told me something that I should have known but didn’t: American companies are required to pay U.S. income tax on interest and dividends earned on their offshore cash, regardless of whether that income is repatriated to the U.S. (For details, ask a tax techie about Subpart F.) That’s something that very few people know, but it’s really important for our analysis.

Act Two Last April, S&P issued a nifty report showing how some big U.S. companies are indirectly using their offshore cash to facilitate cheap borrowing in the U.S. That’s the practice that S&P dubs, quite cleverly, “synthetic cash repatriation.” In case you’re interested—and you should be—offshore cash is 60% of the total cash that S&P-rated companies had on their books as of June 30, up from 44% at year-end 2009.

If the interest rates at which a company invests its surplus cash offshore and borrows in the U.S. for projects here were identical, the offshore interest income would totally offset the U.S. interest expense. But in the real world, the money a company would borrow to fund a productive, job-creating project would typically have a longer maturity than the short-term securities in which firms generally stash their offshore cash. Therefore, money borrowed in the U.S. to fund a project here would carry a higher interest rate than what the offshore cash earns.

So let’s say a company is earning 1% on its offshore cash and pays 3% to borrow here. After taxes—remember, interest paid in the U.S. is deductible to the borrower—that 2% spread costs the company only 1.3%.

Act Three The grand finale: A big company that wants to make a capital investment in the U.S. typically has a “hurdle rate”—a minimum return that it expects to earn on that investment—of at least 10% after taxes.

If an investment isn’t likely to earn at least the hurdle rate return, the company probably won’t make it, regardless of where the cash to pay for it comes from. If the projected profit exceeds the hurdle rate, the company will make the investment. Shelling out 1.3% after tax to finance an investment expected to earn double digits after tax is a no-brainer.

Using offshore cash to borrow cheaply in the U.S. strikes me as a better long-term deal for shareholders than having a company shell out big money to buy an inversion partner, and then having to make that corporate marriage work. (The acquisition has to be sizable, relative to the inverter’s stock market value, for the deal to qualify for inversion treatment under the tax code.)

There’s no question that a 1.3% annual cost makes “financial engineering” maneuvers, such as using U.S. borrowings to pay dividends and buy back shares, less lucrative for shareholders than they would otherwise be. However, as we’ve seen, if a company wants to use synthetically repatriated cash to expand and grow, that 1.3% isn’t a big deal.

My conclusion: the idea that a U.S. company with offshore cash has to invert and desert our country in order to make an investment here is nonsense. Up with intelligent borrowing. Down with whining.

This is an expanded version of a column that will appear in the November 17, 2014 issue of Fortune.