Tomorrow is the first Friday of October, which means the Labor Department will release its monthly jobs report, an updated look at how many jobs the economy added and where the unemployment rate stands.

This so-called jobs report has been of great interest to the public in the years following the recession. After all, the unemployment rate hit a nearly 30-year high in 2009 and, since that point, the economy has added jobs at slower pace than during any economic recovery in recent memory. During the run up to the 2012 elections, the report had major political implications, as political analysts repeatedly told us that the unemployment rate was an important indicator of President Obama’s reelection chances.

But between the 2012 elections and today, a funny thing has happened: the jobs market has more or less recovered by conventional measures. On Thursday morning, the Labor Department announced that the number of newly jobless people who applied for unemployment benefits fell this week to 287,000—the lowest reading in 14 years. Meanwhile, the unemployment rate sits at 6.1%, which is below the average reading over the past 20 years. The unemployment rate is so low that some members of the Federal Reserve believe that we’re close to reaching the “natural rate of employment,” or the level economists estimate is about as low as you can get without stoking inflation.

Yet, at the same time, a whopping 72% of Americans believe we are still in a recession, according to a recent poll from the Public Religion Research Institute. So how do we reconcile these two very different trends?

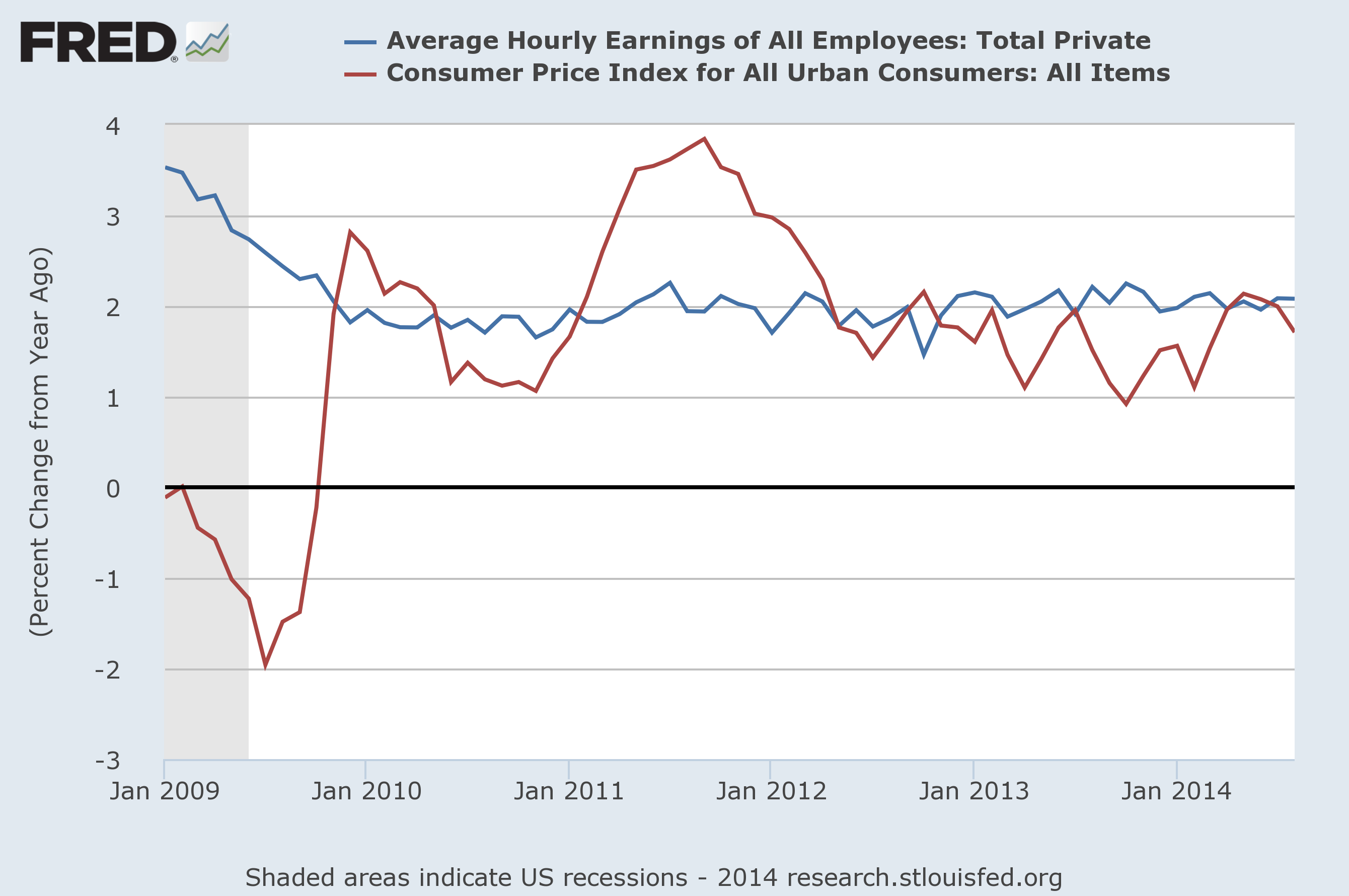

The total number of jobs created, which had been a good enough metric to estimate the state of the economy, just isn’t cutting it anymore. The number we need to be looking at, which is also released in the monthly Employment Situation Report, is income. And unlike the jobs picture, there’s been little to no improvement when it comes to average hourly earnings:

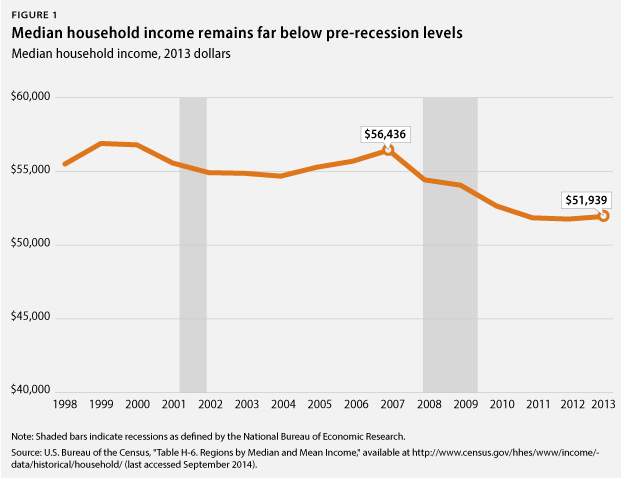

As you can see, since the economic recovery began, average hourly earnings have only kept up with inflation. And without rising incomes, there’s little reason for people to feel like their lives are getting better or for the economy to grow at a faster rate. The picture looks even worse when you focus on the middle class. The Census Bureau released data this week showing that the median household income (a better representation of the typical family than average earnings) didn’t rise at all in 2013. In fact, by this measure, the typical family is doing worse since long before the recession:

The chart above, from the Center for American Progress, shows just how long the ordinary American family has been running in place. These trends were easy to ignore during the real-estate-bubble years, when families could compensate for stagnant incomes with home equity loans. But today, all of this has become painfully obvious to Americans.

Policy makers and the media should be paying attention to income, not jobs. It’s great that there are many more people employed today than four years ago, but it’s time to focus on America’s income problem.